The Ticker Analysis

Hold the Line — The Signal Still Says Stay Invested

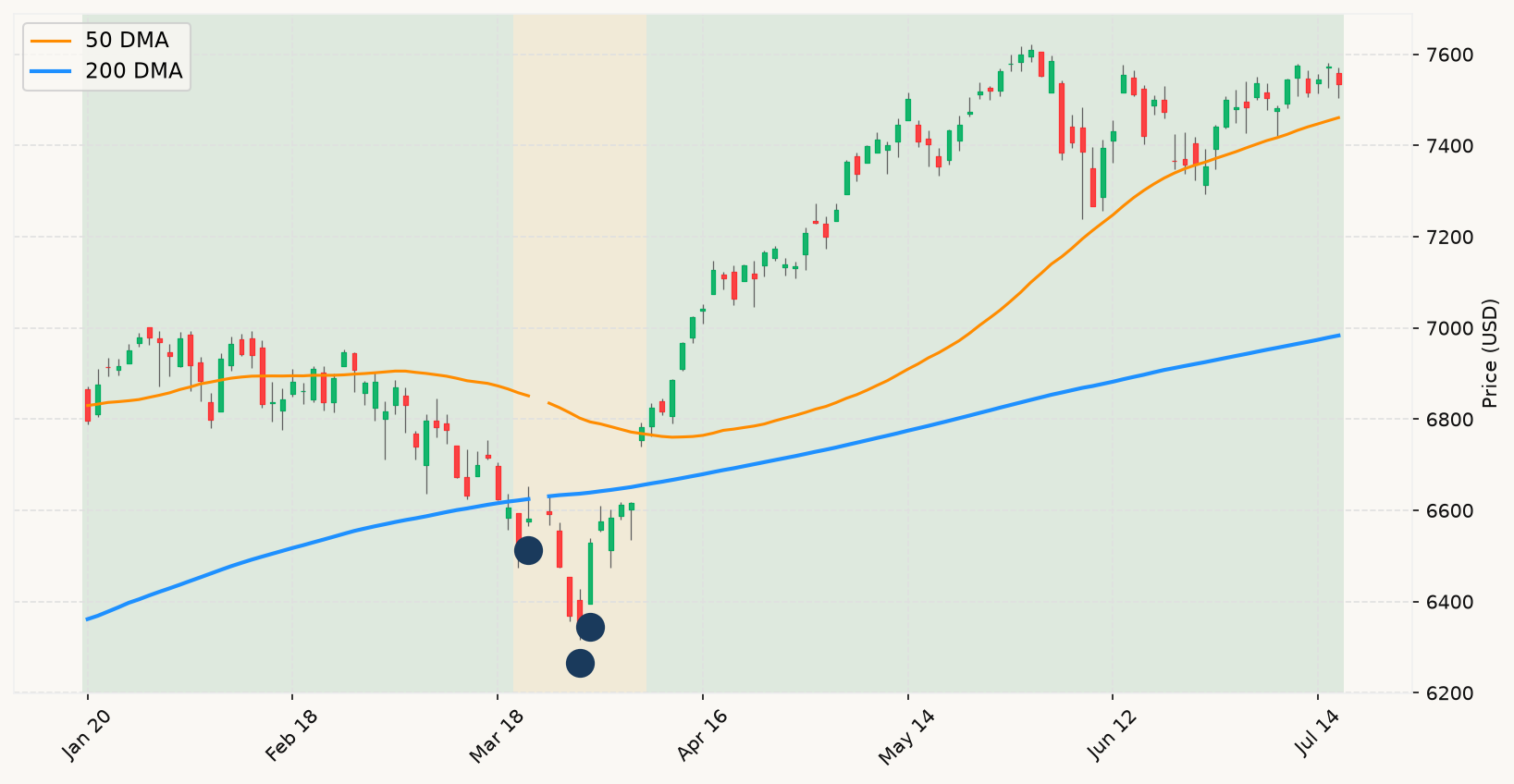

The semiconductor rout and Netflix guidance miss are generating substantial noise, but the correct analytical response is to separate the sentiment from the signal. The primary market trend is squarely bullish — the S&P 500 remains well above its long-term trend line, sitting less than 1% from an all-time high set just 45 days ago. When the broadest measure of U.S. equity health is operating at that altitude, corrections in individual sectors — even dramatic ones like the chip selloff — are a feature of bull markets, not a warning that the regime is changing. Crowded trades unwind; that is normal. The question is whether the damage is spreading into the index itself in a sustained, grinding way. It is not. The broader tape has held up while semiconductors have taken the hit, with defensive sectors like healthcare and consumer staples actually outperforming Thursday — classic rotation behavior, not capitulation.

The recession confirmation signals remain clean. The interest rate environment, while no longer a tailwind after Jefferson's hawkish lean, is not flashing the inversion that has historically preceded every modern recession. The spread between long and short rates is positive and holding. Labor market signals show no deterioration — the employment conditions backdrop remains firm with no triggering of the unemployment-rate threshold that would constitute a genuine recessionary alarm. The real-time growth picture has moderated from its early-Q2 peak but remains positive. Multiple leading indicators would need to turn simultaneously and sustain deterioration before the framework would call for any defensive repositioning. None of that convergence is present right now. The bear case requires evidence, and the evidence isn't there.

The Middle East escalation and the new Brazilian tariff threat are the kinds of geopolitical and trade headlines that feel urgent and market-moving in the moment but almost never alter the primary trend in isolation. The market has known about the Iran conflict for weeks and has priced it accordingly — oil is elevated, defense names are bid, and the broader index has digested the news without breaking down. Jefferson's rate-hike comment deserves slightly more attention because it speaks directly to the monetary policy outlook, but he explicitly did not endorse a hike at the upcoming meeting, and "open to hiking later if needed" is a conditional statement, not a pivot. The interest rate environment remains accommodative relative to where it was at the peak of the 2022 tightening cycle, and monetary policy signals are not yet restrictive enough to be materially impairing corporate earnings capacity.

For a fully invested long-term equity holder, the correct posture today is unchanged: stay put. The decision matrix resolves cleanly — the market is above its primary trend, the all-time high is recent, no recession signals are converging, and the velocity of any decline from the ATH is minimal at just 1%. The AI spending debate is real and will continue to create volatility in individual names and sectors, but that is a stock-picker's problem, not an index investor's problem. The investor who owns the broad market owns every winner that emerges from this AI buildout, regardless of which names ultimately deliver — and does so without the catastrophic single-stock risk that Netflix holders absorbed overnight. The noise is loud today. The signal says hold. MoreLess