The Ticker Analysis

Bulls Hold the Line Despite AI Wobble & Oil Shock

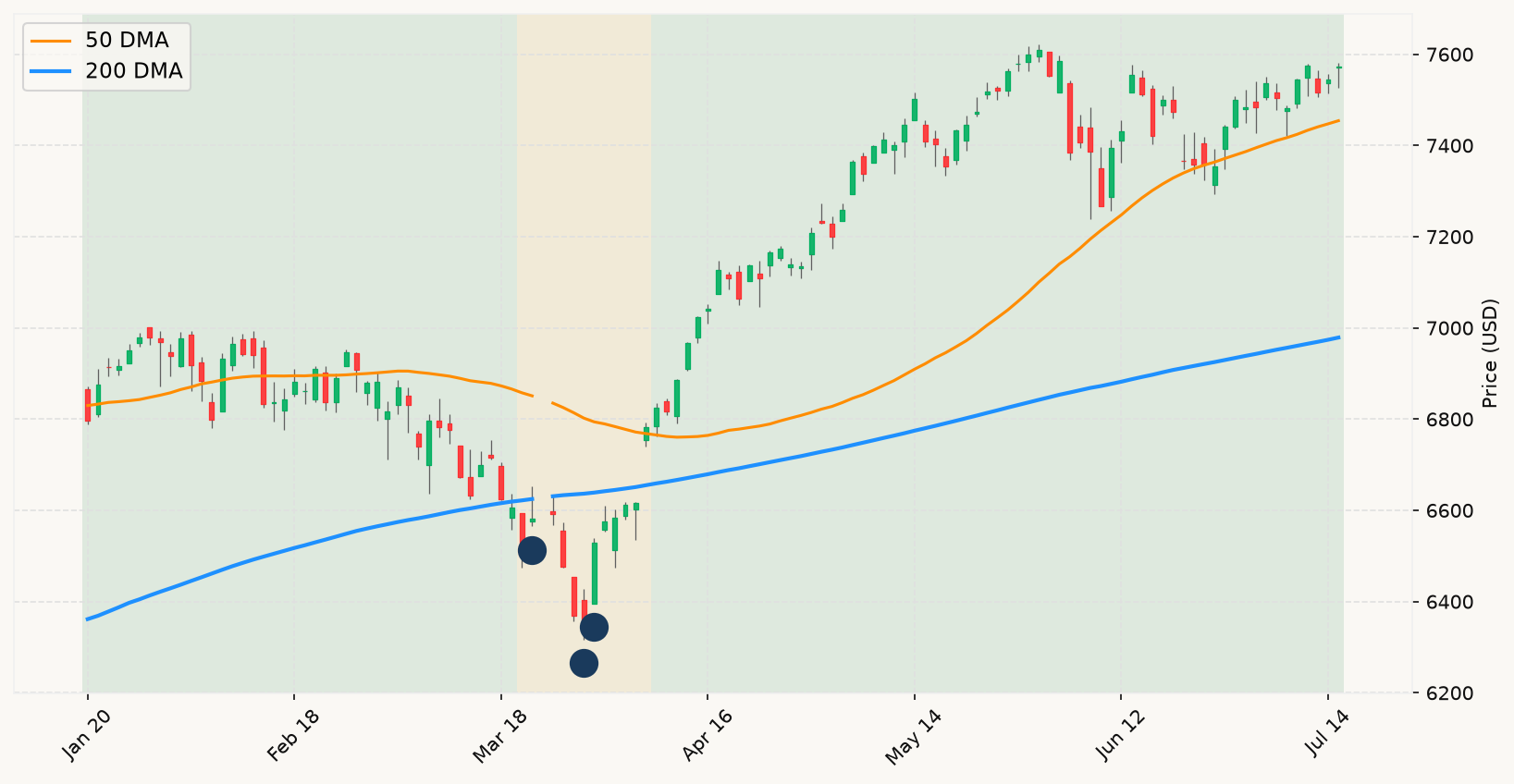

The TSMC earnings story is classic signal-vs-noise territory — and the verdict here is noise, at least from a big-picture positioning standpoint. TSMC delivered a genuine beat on revenue and the AI demand picture it painted is consistent with a healthy, expanding cycle. The selloff in chip stocks isn't a market sending a distress signal; it's the normal friction of a momentum trade hitting a near-term air pocket. The primary market trend is firmly bullish — the S&P 500 is trading well above its long-term trend line, sitting a whisker from all-time highs. The velocity of any current softness doesn't come close to the kind of grinding, slow deterioration that historically precedes a recessionary bear. Fretting over a one-day AI trade wobble while the broader market is near record levels is exactly the kind of noise that gets investors in trouble.

The June CPI print deserves more analytical weight, and its message is constructive. A meaningful deceleration in headline inflation — driven by energy reversals tied to the brief ceasefire — combined with cooling core readings gives the Fed room to hold at the upcoming July FOMC meeting. New Chair Warsh has made clear he's data-dependent, not forward-guidance dependent, which means the interest rate environment remains conditionally benign: rates stay on hold until the data forces the issue. A hold is a bull-market backdrop. The risk is that renewed oil price surges from the re-escalating Iran situation push energy back into the headline number in July and August — but that's a future data problem, not a present one. Right now, the monetary policy signals are not moving toward convergence with any other recessionary indicators. That's important. Both legs of the diagnostic have to fire for this framework to call a bear market, and neither is firing.

The Iran-Hormuz situation is the most legitimate macro risk in the current picture, and it's worth watching through a specific lens: not as a geopolitical narrative, but as a potential driver of the economic indicators that actually matter. If sustained oil shocks reignite core inflation, force Fed hikes, and begin grinding into corporate margins and consumer spending simultaneously, the leading indicators start moving. If that happens while the stock market shifts from its current near-ATH posture into a slow, grinding decline, the diagnostic framework begins to register. Right now, none of that has happened. Oil is spiking, but the market isn't confirming a systemic deterioration — it's near record highs, not in a downtrend. The geopolitical narrative is scary; the market's verdict thus far is that it's manageable.

The bottom line for a fully invested equity holder is straightforward: stay the course. Employment conditions remain solid, monetary policy signals are not flashing contraction, and the stock market trend is unambiguously bullish. The current episode — an ATH-proximity market with an AI trade wobble, a hot geopolitical story, and a Fed in wait-and-see mode — maps precisely to the 80% base case: a market in a healthy bull trend experiencing routine friction. The historical record is emphatic that the investors who get hurt in this environment are the ones who mistake noisy headlines for structural deterioration and move to the sidelines, only to watch the recovery happen without them. The burden of proof is on the bear case. That proof has not arrived. MoreLess