The Ticker Analysis

Bull Trend Intact — Iran & Oil Are Just Noise

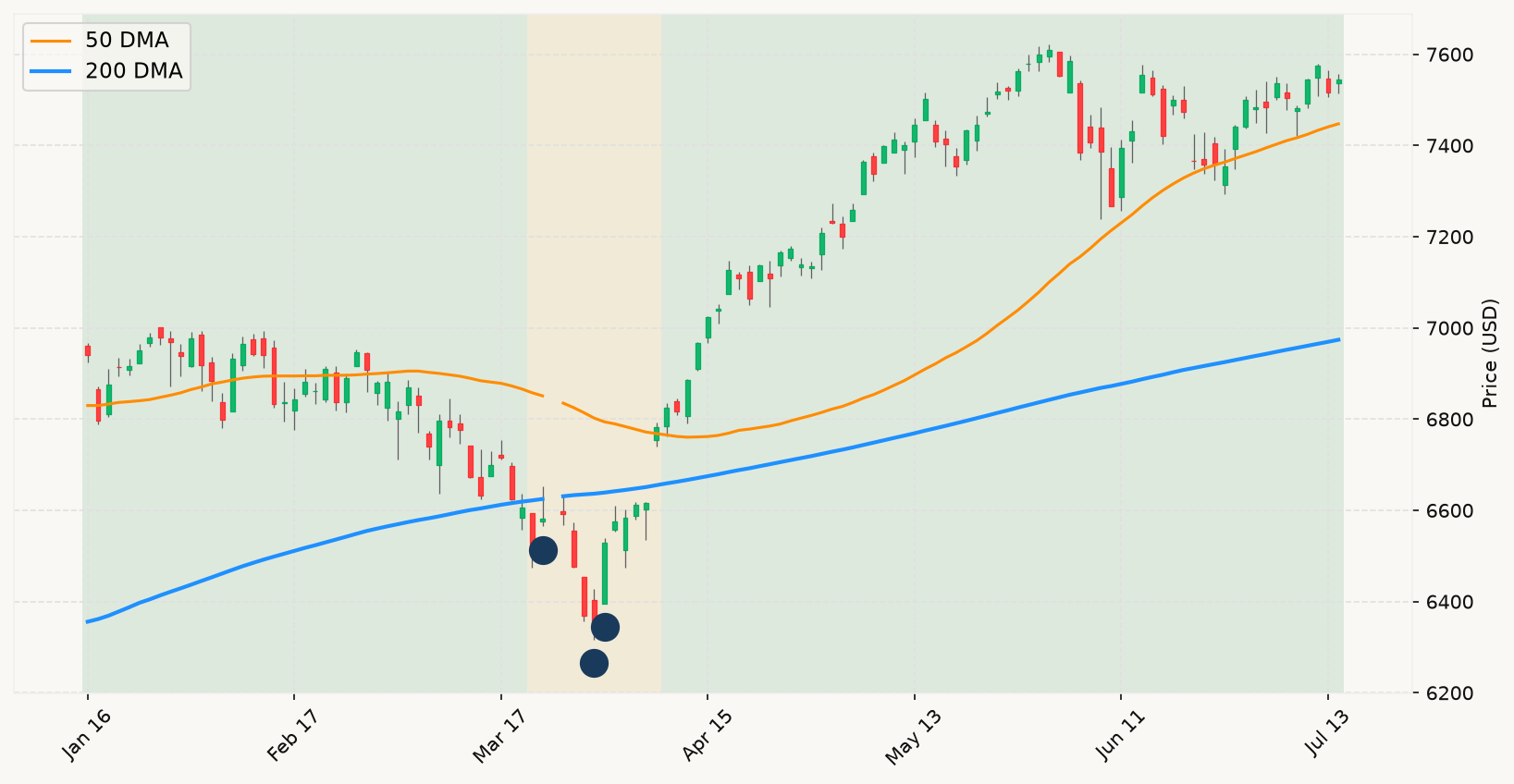

Today's twin inflation prints — a sharply lower CPI yesterday and a surprise PPI decline this morning — are the most market-relevant news of the week, and the framework's verdict is straightforward: noise. Not because inflation data is unimportant in the abstract, but because the market is already well above its primary trend, sitting comfortably above a stock market trend that has been confirming the bull case for months. When the primary trend is intact and the market is near all-time highs, individual data releases — even genuinely good ones — don't change the regime diagnosis. The market was already pricing in a resilient economy. Today's prints confirm that picture; they don't create a new one.

The Iran escalation deserves a more careful read, but the framework's answer here is also clear. Geopolitical shocks of this type — sudden oil spikes, naval blockades, regional military exchanges — have a consistent historical signature: they produce sharp, sentiment-driven volatility that the primary trend usually absorbs without a structural break. The 80% base rate applies here with force. What makes a shock matter is not its headline severity but whether it is producing a slow, grinding deterioration in the primary trend paired with converging deterioration in leading economic indicators. Neither condition is present. The stock market trend remains solidly bullish, the interest rate environment is showing a normal, positively sloped curve, employment conditions remain healthy, and the growth nowcasts are both positive. A 15% oil spike over three days, however alarming in the news cycle, does not move any needle in this analytical framework.

The Morgan Stanley blowout and the broader bank earnings wave this week are worth noting for what they confirm rather than what they change. Record revenues and EPS across the major financial institutions — the sector most sensitive to credit conditions, economic activity, and capital markets health — is about as clean a real-time validation of the bull thesis as you can get. Active markets, robust investment banking pipelines, and strong fixed income results collectively tell you that the underlying economic machinery is functioning well. This is consistent with everything else the framework sees: a market in confirmed bull territory, a positively sloped rate curve, and no recessionary convergence signals in sight.

The one genuine watch item is the feedback loop between Iran and inflation. The June CPI number was almost entirely an energy story — the ceasefire drove oil down, which drove prices down. That ceasefire is now over, and oil is surging. If Brent stays elevated through July and into August, the next CPI print will likely reverse much of this month's relief, putting Chair Warsh back in a hawkish posture and re-energizing rate-hike expectations. That scenario would be worth monitoring through the lens of what it does to the primary market trend — not through the inflation headline itself. As long as the market continues to hold above its primary trend and economic signals remain healthy, the prescribed posture doesn't change: stay fully invested, and treat the noise for what it is. MoreLess