The Ticker Analysis

Hormuz Shock Is Noise — The Bull Trend Holds

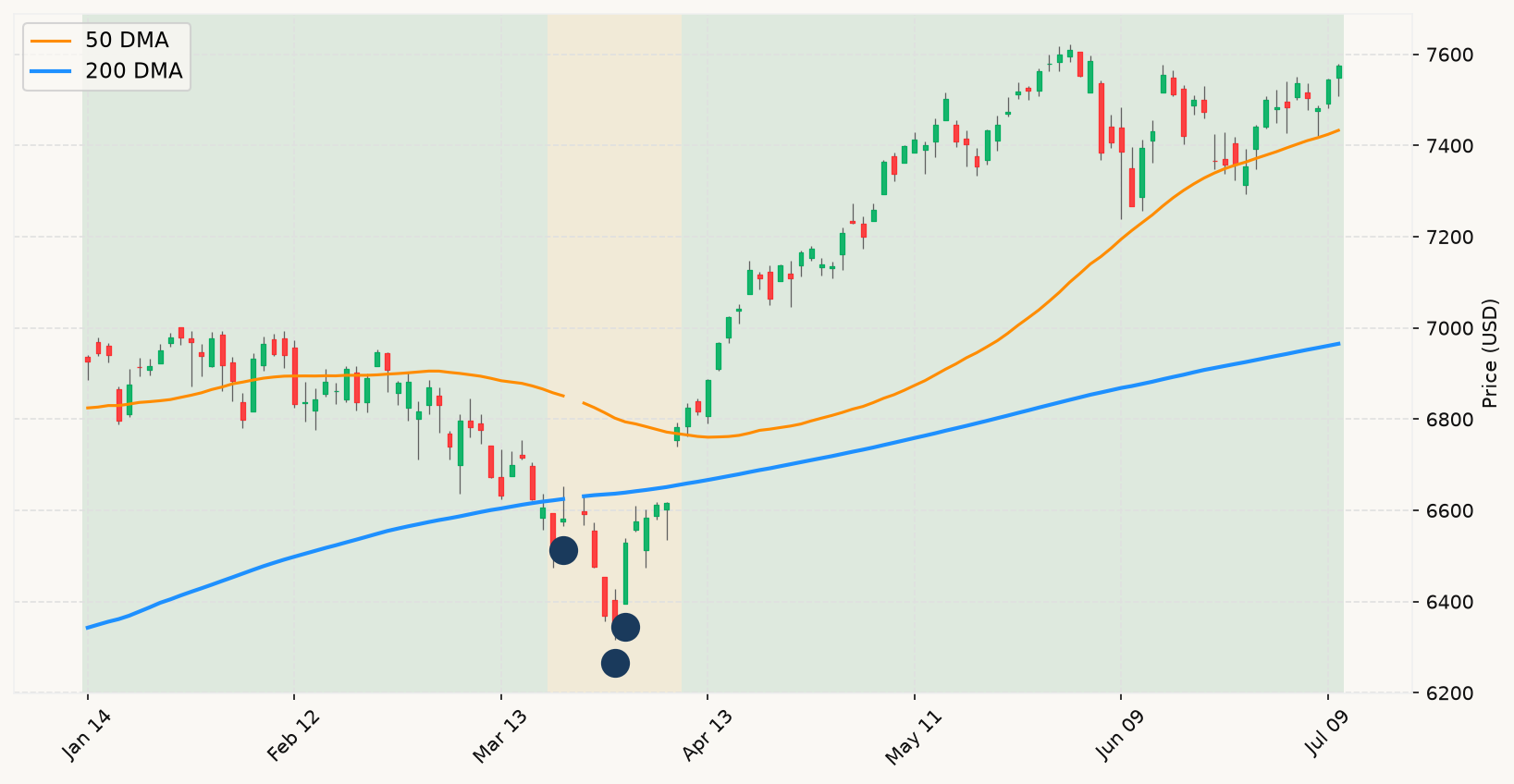

The Iran-Hormuz crisis is the loudest story in the room right now, and the first question to answer is: does it move any needle that matters for long-term equity positioning? The honest answer is that it creates real near-term turbulence — oil up hard, chip stocks selling off, futures mixed — but the primary market trend remains firmly intact. The S&P is comfortably above its long-term trend line, sitting less than half a percent from an all-time high reached just six weeks ago. That is not the setup of a market in distress. That is a bull market absorbing a geopolitical shock in real time, which is exactly what bull markets do.

The geopolitical risk is genuine but familiar in structure. Energy supply shocks rattling markets while the underlying economy continues to expand is a pattern with a long historical track record — and that track record argues against treating headline-driven volatility as a structural inflection point. What would actually change the assessment is a sustained, grinding decline in equity prices paired with deteriorating leading economic indicators. Neither condition is present. Employment conditions remain healthy, monetary policy signals are tilted bullish despite the hawkish Fed chatter, and both growth nowcasts are comfortably in positive territory. The convergence of bearish signals that historically precedes a genuine recessionary bear market is simply not there.

The Fed policy uncertainty this week — Warsh's testimony, the June CPI print, the September hike probability — is the kind of event that generates enormous financial media coverage while historically producing very little durable signal. Markets have navigated "will they or won't they hike" cycles many times. What matters is whether tightening actually tips the economy into contraction. With labor markets solid and growth tracking positive, that threshold is not close. The Q2 earnings picture, with 20%-plus growth now expected for a second straight quarter, reinforces that corporate America is in expansion mode, not contraction. A market near record highs built on genuine earnings growth rather than multiple expansion — as multiple strategists have noted this week — is a far more durable bull than one levitating on sentiment alone.

The SK Hynix selloff and the broader memory-chip weakness deserve a watchful eye for what they signal about AI trade sentiment, but a single sector rotation or post-IPO hangover is noise, not signal. The AI capex story remains intact — TSMC's record revenue is the data point that matters for the structural demand thesis, not one chipmaker's post-debut give-back. For investors with properly diversified index exposure, the correct posture this week is the same as it was last week: stay fully invested, let the headlines do their thing, and keep your eyes on the two indicators that actually matter — where the primary market trend sits and whether economic conditions are deteriorating in a convergent way. Right now, both point the same direction: stay in. MoreLess