The Ticker

Bull Market

The market's cruising at altitude with the engines humming — AI chips popping, airlines printing money, and the bulls firmly in the driver's seat, even as a few storm clouds flicker on the horizon.

Top Story

SK Hynix Lands on Nasdaq in Biggest-Ever Foreign IPO as AI Trade Roars Back

South Korea's SK Hynix made its long-awaited Nasdaq debut today in the largest U.S. listing ever by a foreign company, raising $26.5 billion in a debut that the market is treating as a real-time referendum on whether the AI infrastructure boom still has legs. After a stretch of semiconductor volatility, investors are watching opening-day demand closely as a signal of where institutional appetite for the AI trade stands headed into the back half of 2026.

The broader earnings picture is turning constructive just as the big-bank reporting season approaches. Delta Air Lines kicked things off this morning by beating estimates on both the top and bottom lines, reinstating full-year guidance, and demonstrating that premium travel demand remains resilient even against record fuel costs. Next week brings a flood of major financial sector reports — JPMorgan, Goldman, Bank of America, Wells Fargo, and Citigroup all report — which will offer the first clear read on credit quality, capital markets activity, and loan demand in the current rate environment.

The Federal Reserve remains the dominant macro overhang. Fed Chair Kevin Warsh's congressional testimony is scheduled for July 14, the same day June CPI prints — a collision of events that could sharply reprice rate-hike expectations in either direction. The Fed held rates steady at its June meeting, but nine of eighteen officials penciled in at least one hike this year, and minutes released July 8 showed a majority flagging upside inflation risks. Markets are currently pricing near-certainty of a hold at the July 28–29 FOMC meeting, but the CPI print next week could scramble that calculus fast.

The geopolitical wildcard persists in the background. Ongoing U.S.–Iran hostilities have kept energy prices elevated and injected a persistent risk premium into markets all week. Reports of U.S. diplomatic "technical talks" with Iran offered a mild relief signal, but the situation remains fluid. Oil price direction from here will have direct read-through to airline margins, consumer inflation, and ultimately the Fed's room to maneuver — making the Middle East situation far more than just a headline risk. MoreLess

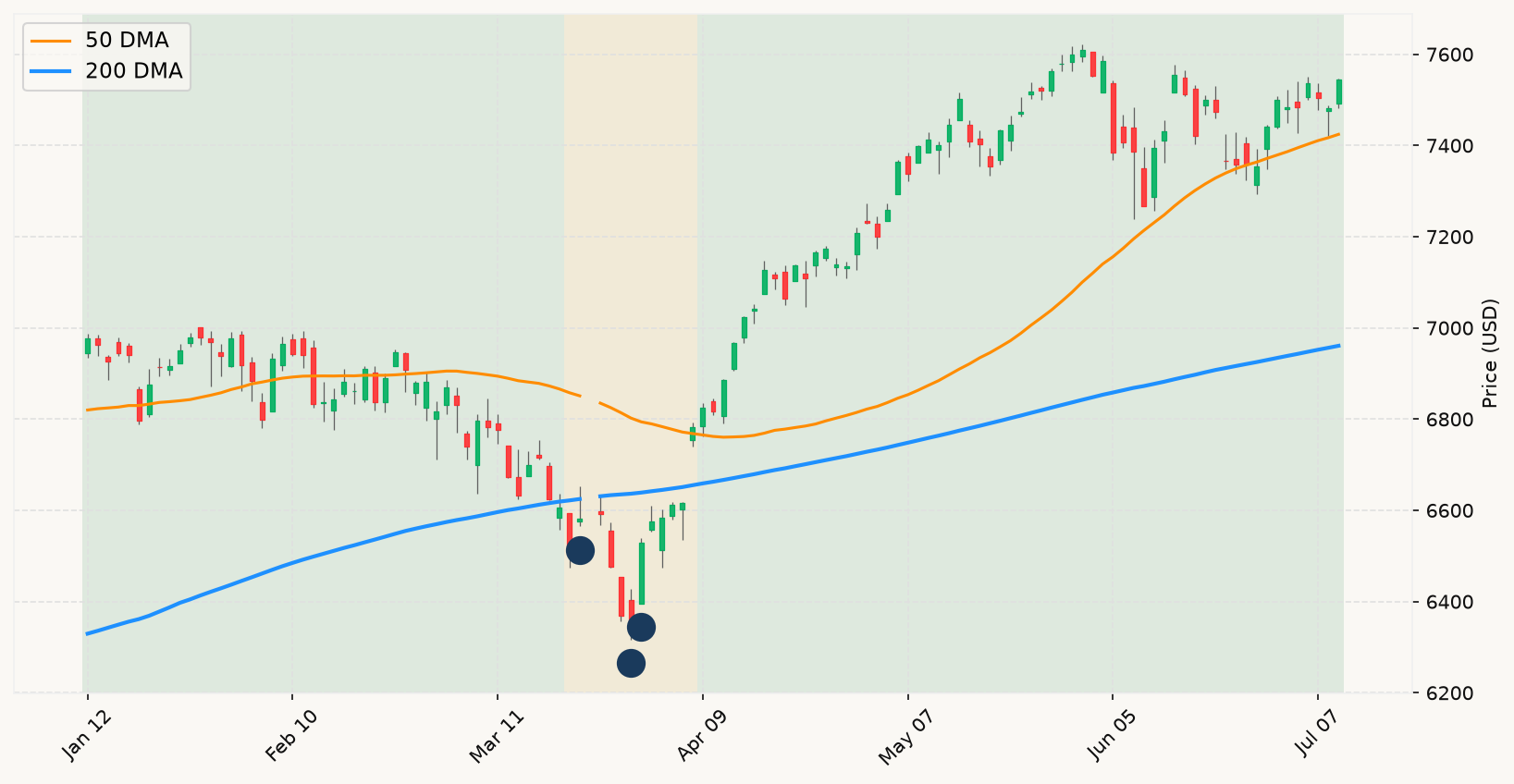

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Market Intact — The Noise Is Just Noise

The dominant story today — SK Hynix's record-breaking Nasdaq debut and Meta's Muse Spark AI platform update — is classic momentum news within an ongoing bull cycle. The primary market trend is firmly bullish: the S&P 500 is well above its long-term trend line, sitting less than 1% from its all-time high. There is no velocity signal, no grinding deterioration, and no technical warning flag of any kind. News that amplifies the AI narrative — whether it's a monster semiconductor IPO or a tech giant rolling out a competitive new model — is the kind of story that arrives during bull markets, not bear markets. Treat it as color, not signal.

Delta's earnings beat is worth noting for what it reveals about the macro backdrop: demand is strong enough that the most profitable U.S. airline absorbed record fuel costs, beat estimates, and reinstated full-year guidance in the same breath. The "K-shaped" consumer dynamic Bastian described — premium demand resilient while cost-sensitive segments feel pressure — is a real structural feature of this cycle, not a warning sign. Earnings season gets considerably more interesting next week when the major banks report. Credit quality, loan growth, and capital markets commentary from JPMorgan and Goldman will be the most informative macro read-through of the quarter. Watch those, not the headlines.

The Fed and inflation picture is the one thread that deserves genuine attention, though the framing matters enormously. Nine FOMC officials penciled in a hike this year, minutes flagged upside inflation risks, and June CPI prints next Tuesday alongside Fed Chair Warsh's congressional testimony. That is a legitimate data cluster to watch — not because any single print changes the regime, but because a hot CPI combined with hawkish Warsh commentary could meaningfully shift the rate-hike probability curve at the short end. Even so, the interest rate environment shows a positively sloped curve — a constructive monetary policy signal — and employment conditions remain solid. The two recession signals that matter are not converging: there is no sustained breach of the primary trend and no broadening deterioration in leading indicators simultaneously. That is the bar that matters.

The Middle East situation — U.S.–Iran hostilities, Strait of Hormuz risk, elevated oil prices — generates daily headlines but has not moved any needle that matters within a disciplined analytical framework. The market has had this information for weeks and is sitting within 1% of its all-time high. If the geopolitical risk were genuinely repricing growth expectations or triggering systemic credit stress, the market would be telling you so through price action. It isn't. The bulls are in control of the tape, the economic signals are not deteriorating, and the base rate argues overwhelmingly for staying fully invested. There is no actionable bear case here — only noise dressed in urgent-sounding clothes. MoreLess