The Ticker Analysis

Geopolitical Fire, But the Bull Trend Holds

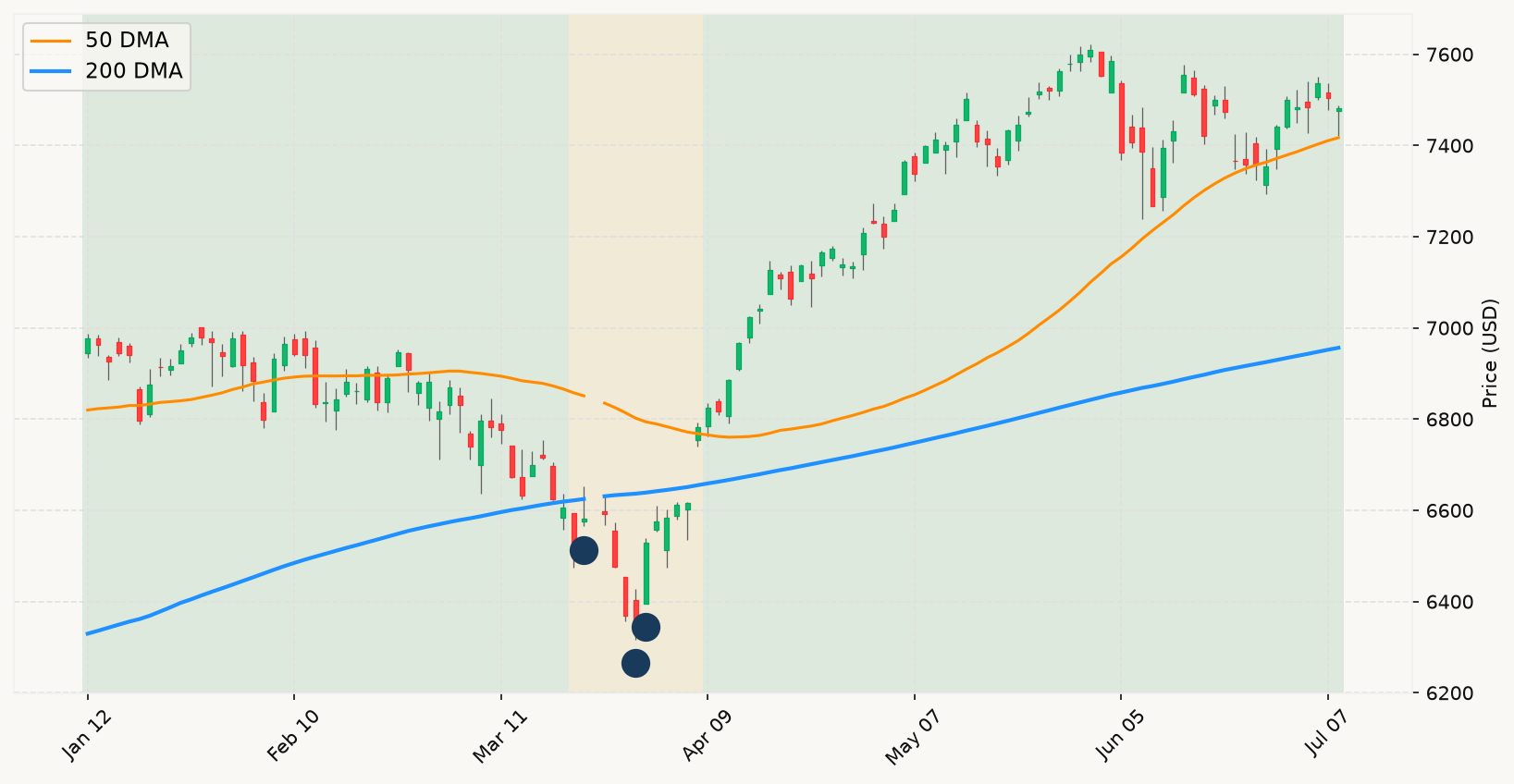

The headline risk today is the U.S.-Iran conflict, and it's worth applying the right lens before reacting. Geopolitical crises are among the most reliably noise-generating events in market history — dramatic in the moment, frequently reversed in their market impact within weeks. The relevant question is not whether this is alarming (it clearly is) but whether it is moving any of the dials that actually matter for the long-term investor. The answer right now is: modestly, and in ways that warrant monitoring rather than action. The market trend remains decisively bullish — equities are well above their long-term primary trend, the drawdown from the all-time high is a rounding error, and there is zero evidence of the slow, grinding deterioration that characterizes the early stages of a recessionary bear market. Geopolitical shocks that do not trigger recession have a historical track record of resolving quickly in equity markets, often with violent V-shaped recoveries that punish those who stepped aside.

The Fed minutes are more substantively interesting, though still not a signal that changes the posture. What they confirm is genuine internal division at the FOMC — hike camp vs. cut camp — under a new chairman who has explicitly signaled he will minimize forward guidance. That uncertainty is real and it will keep the interest rate environment in a state of productive ambiguity through the July 29 meeting and into the fall. A potential rate hike is on the table, which applies a headwind to rate-sensitive sectors. But a divided Fed that is data-dependent is not a Fed that has lost control — it's a Fed watching the same inflation-versus-growth tension the market is watching. The spread between the 10-year and 3-month yields remains comfortably positive, meaning the interest rate environment is not flashing the warning sign that precedes recessions. That matters more than whatever the minutes say about the internal debate.

The economic signals outside of geopolitics are genuinely mixed, but not alarming. The Atlanta Fed's real-time growth estimate has slid from robust levels earlier in the quarter to a more modest reading — reflecting the same energy price shock and trade disruption that's in the headlines. But modest positive growth is still positive growth. Employment conditions are flagging some softness — June payrolls badly missed expectations — but the unemployment rate actually ticked down, and there is no sign of the kind of broad, accelerating deterioration that the historical record associates with recession onset. PepsiCo's beat-and-reaffirm this morning, combined with SK Hynix's oversubscribed ADR and Amazon's $25 billion AI infrastructure bet, suggests corporate conviction is not cracking. Earnings season is young, but the opening hand is not bearish.

The bottom line for a fully invested equity holder is straightforward: stay the course. The market is above its primary trend, the all-time high was set just over a month ago, and every signal in the economic leading indicator set is either neutral or mildly positive. The Iran situation is a legitimate wildcard — if it generates a sustained oil shock that meaningfully accelerates inflation and tips the Fed decisively toward hikes, that changes the picture and warrants a reassessment. But that is a conditional future scenario, not the current evidence. The historical base rate is clear: the overwhelming majority of geopolitically-driven market scares resolve without becoming sustained declines, and the investors who exit in the early days of a crisis most frequently miss the recovery. Nothing in today's data justifies abandoning that base rate. Watch the oil price trajectory, watch the July 14 CPI print, and watch what the employment picture does over the next sixty days. Until those needles move materially, the correct posture is patience. MoreLess