The Ticker Analysis

Stay the Course — The Signals Are Green

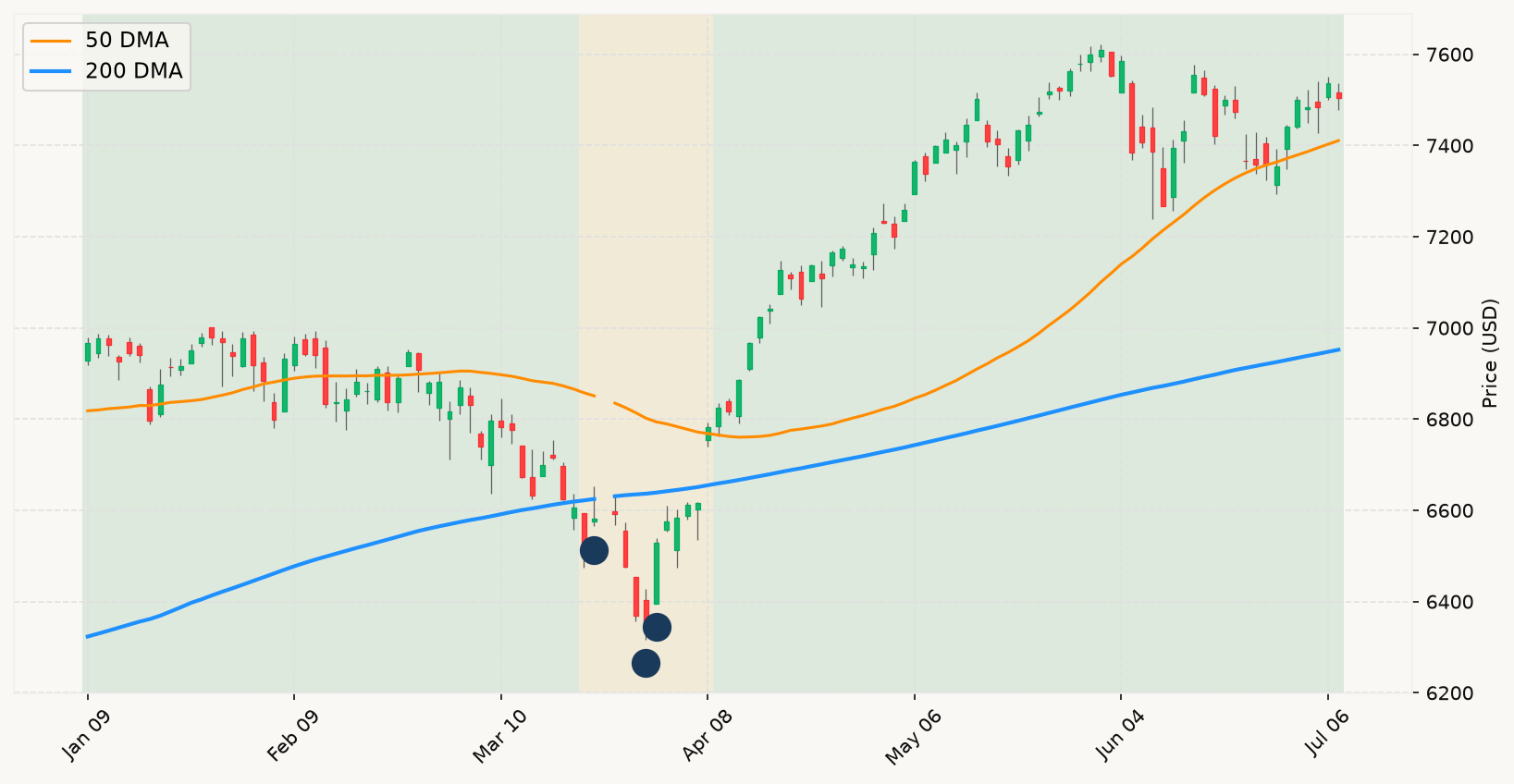

The Iran escalation is the loudest headline this morning, and the instinct to treat it as a reason to reposition is understandable — but the analytical case for doing so is weak. Geopolitical shocks of this variety are textbook noise within a rigorous market framework. The mechanism is simple: oil spikes, risk assets sell off, headlines scream danger. But the actual question — does this change the primary market trend or move any leading economic indicator meaningfully toward recession confirmation? — almost always comes back no. The S&P 500 remains comfortably above its long-term stock market trend line, which is the load-bearing signal in any assessment of regime. Until that changes on a sustained basis, the default posture is fully invested, and a morning futures selloff driven by geopolitical fear does not alter that verdict. Every major geopolitical shock in the dataset — including conflicts with far more direct economic exposure than this one — resolved without triggering a sustained breach of the primary trend absent a concurrent recession. This is Noise. Delivered without apology.

The FOMC minutes landing today deserve more attention than the Iran headlines, but the framework's verdict is the same. Markets already know the June meeting carried a hawkish lean — nine officials penciling in a hike, rates held at 3.50–3.75%. The minutes provide color, not new information. What actually matters is whether the interest rate environment deteriorates to the point where the 10-year/3-month spread inverts — and right now it sits in positive territory, a configuration that historically carries no recession signal. The Fed holding rates elevated is not inherently bearish for equities; it is only bearish when combined with a deteriorating growth picture that the market begins pricing in through a grinding, gradual decline. That combination is not present. The stock market trend remains intact. Rate-hike anxiety is a narrative. The spread is the signal.

The earnings setup — 23% projected year-over-year growth for Q2 — is the kind of figure that generates both excitement and anxiety, and the framework is clear on how to treat both. Strong earnings are already priced in. A beat does not produce a durable signal; neither does a miss, unless the miss is so broad and sustained that it begins moving the growth nowcasts materially lower. What is worth noting is that the Atlanta Fed's Q2 GDPNow sits in positive but moderating territory — the economy is not contracting, but the growth rate has softened from earlier in the quarter. This is the kind of early-stage deceleration worth monitoring across multiple indicators simultaneously. None of the leading economic indicators are in convergence toward a recessionary signal right now: employment conditions remain solid, monetary policy signals are not flashing inversion, and the stock market trend is above the primary line. The bar for a bear market ruling remains very high, and nothing in today's news clears it.

The positioning implication is straightforward: stay fully invested. The market is above its long-term trend line, the drawdown from the all-time high is negligible, and there is no convergence of recessionary signals. The Iran shock and the Fed minutes are generating volatility and narrative, but volatility and narrative are not the framework's inputs — price trend and economic confirmation are. The 80% base rate says that even in the event of a deeper pullback, corrections resolve far more often than they become prolonged bears. With every confirming indicator pointing in a bullish direction, this is not a moment for hedging or defensiveness. It is a moment for recognizing that the scariest-feeling environments near all-time highs, when geopolitical headlines are dominating the tape, are historically some of the most rewarding periods for investors who stay put. The data says ride it. MoreLess