The Ticker Analysis

All Green — Tune Out the Noise and Stay Put

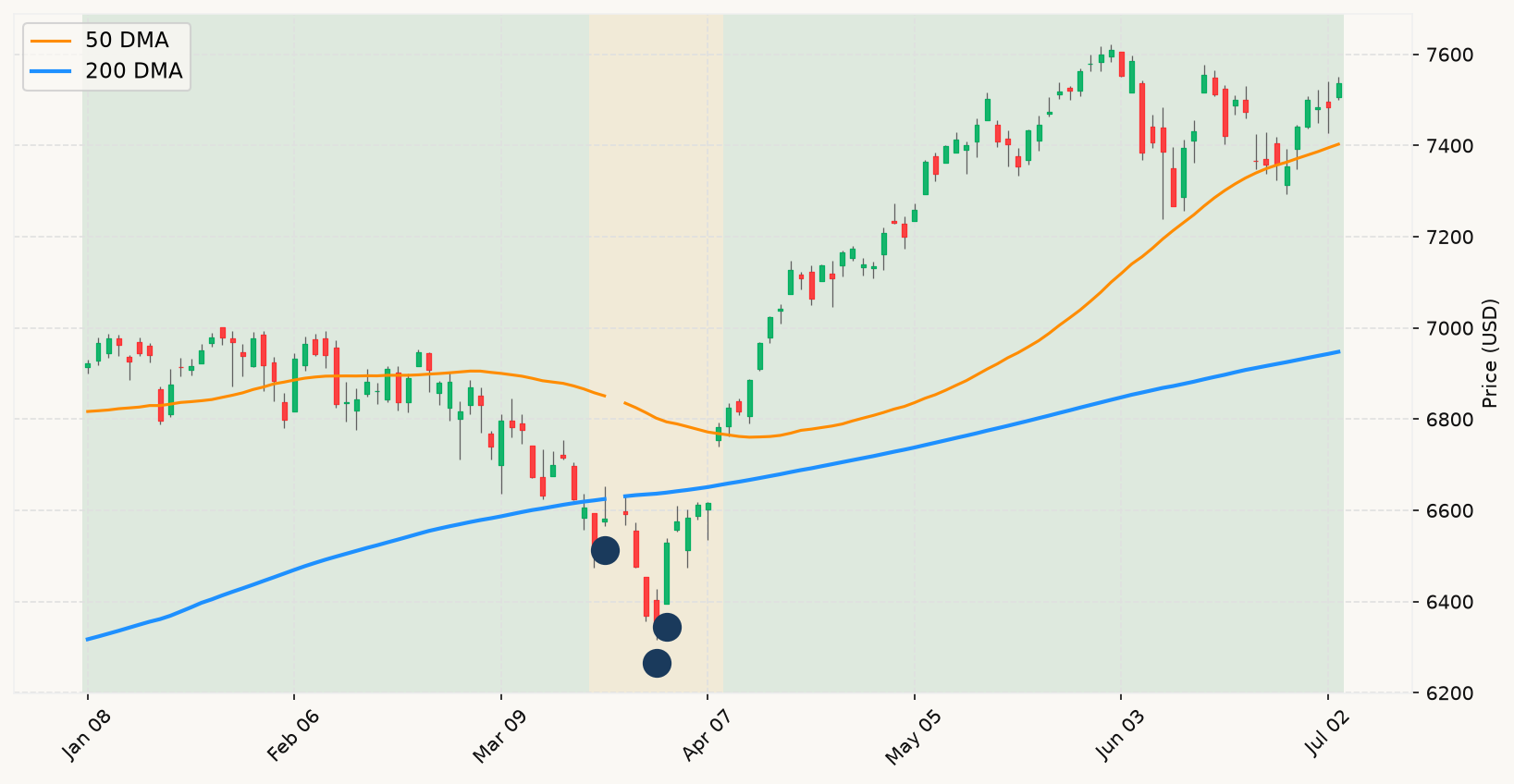

The Samsung earnings episode is textbook noise, and the chip selloff cascading from it deserves the same label. A company reports a 19-fold profit surge and gets sold — that is a sentiment and positioning story, not a fundamental deterioration story. The market was crowded in AI hardware names, expectations had run ahead of results, and fast money rotated out. This kind of sector-level air pocket happens routinely in bull markets, and the primary market trend — which is firmly bullish with equities sitting well above their long-run trend line — renders these episodes irrelevant to positioning decisions. Nothing about Samsung's actual results changes the economic picture. The recession confirmation checklist has not moved: the interest rate environment remains positive, with the yield spread solidly in expansion territory, and employment conditions — despite the soft June payroll print — show no signs of the kind of broad deterioration that would constitute a recessionary signal. One soft month, with unemployment still sitting at 4.2%, is not a labor market alarm bell. It is data.

The June NFP miss is the week's most consequential data point from a macro framework perspective, and the correct read is that it is incrementally constructive for the bull case, not a warning sign. A labor market that is cooling without collapsing is precisely the soft-landing script. The Sahm-rule-equivalent deterioration that would signal genuine recessionary labor market stress requires a sustained, meaningful rise in unemployment from its recent low — and that is not what the June data shows. What it does show is that the Fed's rate-hike urgency has been dialed back by markets in real time: September is off the table, the hawks have less ammunition, and the pressure on equity multiples from further tightening has eased. That is a tailwind, not a headwind. The monetary policy signal from the interest rate environment was already bullish — this data point reinforces it.

SpaceX's Nasdaq-100 inclusion is structural noise dressed up as a catalyst. The billions in forced passive buying are a mechanical index-rebalancing event. It creates intraday volatility in QQQ and SPCX, but it does not change the earnings trajectory of the index, the health of the economy, or any signal that the analytical framework tracks. The same logic applies to the bank earnings parade this week. JPMorgan's blowout, and whatever Goldman, Wells Fargo, Citi, and BofA deliver, will generate enormous headline flow. The framework's position on earnings is clear: they are lagging indicators, already priced in before announcement, and systematically over-extrapolated during both bull and bear phases. A strong bank earnings week does not change the primary trend status. A weak one does not either — unless it triggers sustained market deterioration that begins reshaping the trend itself.

The current positioning prescription is unchanged and unambiguous: stay fully invested. Every signal that matters is green. The stock market trend is bullish. Employment conditions are stable. The interest rate environment is constructive. The nowcast data shows positive growth. The drawdown from the all-time high is less than 1%, which puts the market essentially at its peak — and historical data is explicit that markets at or near all-time highs have delivered above-average forward returns, not below-average ones. The temptation to read the Samsung selloff, the chip rotation, or the soft jobs print as early warning signs of something larger is exactly the kind of narrative-driven error the data argues against. The noise machine is loud this week. The signal is quiet — and quiet signals in a confirmed bull market mean stay put. MoreLess