The Ticker

Bull Market

The bulls are lounging in lawn chairs, sipping lemonade, and watching fireworks — it's a holiday weekend cookout with good food, easy breezes, and not a storm cloud in sight.

Top Story

Soft Jobs Report Knocks Fed Hike Odds, Lifts Markets Into Holiday

The U.S. economy added just 57,000 jobs in June — roughly half of what Wall Street expected — and the miss landed with an immediate market pop as traders rapidly repriced the odds of a Federal Reserve rate hike this fall. Stock futures moved higher, Treasury yields slipped, and the September hike that markets had been pricing at better than 50% odds was taken largely off the table in the minutes after the report hit.

The jobs data arrive against a backdrop of a market that has already had a strong 2026. U.S. indexes wrapped their best first half since at least 2021, with broad earnings growth from technology, communications, and financials doing the heavy lifting. The second-quarter reporting season is just weeks away and will be the next real test of whether the rally has fundamental underpinning — or whether elevated valuations need the cover of continued profit expansion to hold.

Fed Chair Kevin Warsh has made clear he won't telegraph his next move, but the June print gives the committee significant breathing room to stay on hold at the July 28–29 meeting. The complicating factor is inflation, which surged to a three-year high of 4.2% as measured by the CPI — well above the Fed's 2% target — fueled in part by the U.S.-Iran conflict and elevated energy costs. Warsh acknowledged inflation risks have eased somewhat as oil prices have retreated, but the Fed remains in wait-and-see mode on whether that relief will persist.

The macro backdrop also features a sharp cooling in real-time growth estimates alongside a softening labor market, while the interest rate environment remains the central variable. Oil's decline toward the high $60s on U.S.-Iran peace progress is the most constructive macro development in weeks, as it simultaneously reduces inflation pressure and eases the squeeze on consumer spending. Whether the June jobs weakness is a one-month blip shaped by seasonal distortions — leisure and hospitality typically bulges in summer — or the opening move of a broader softening trend will be the key question markets spend the next several weeks trying to answer. MoreLess

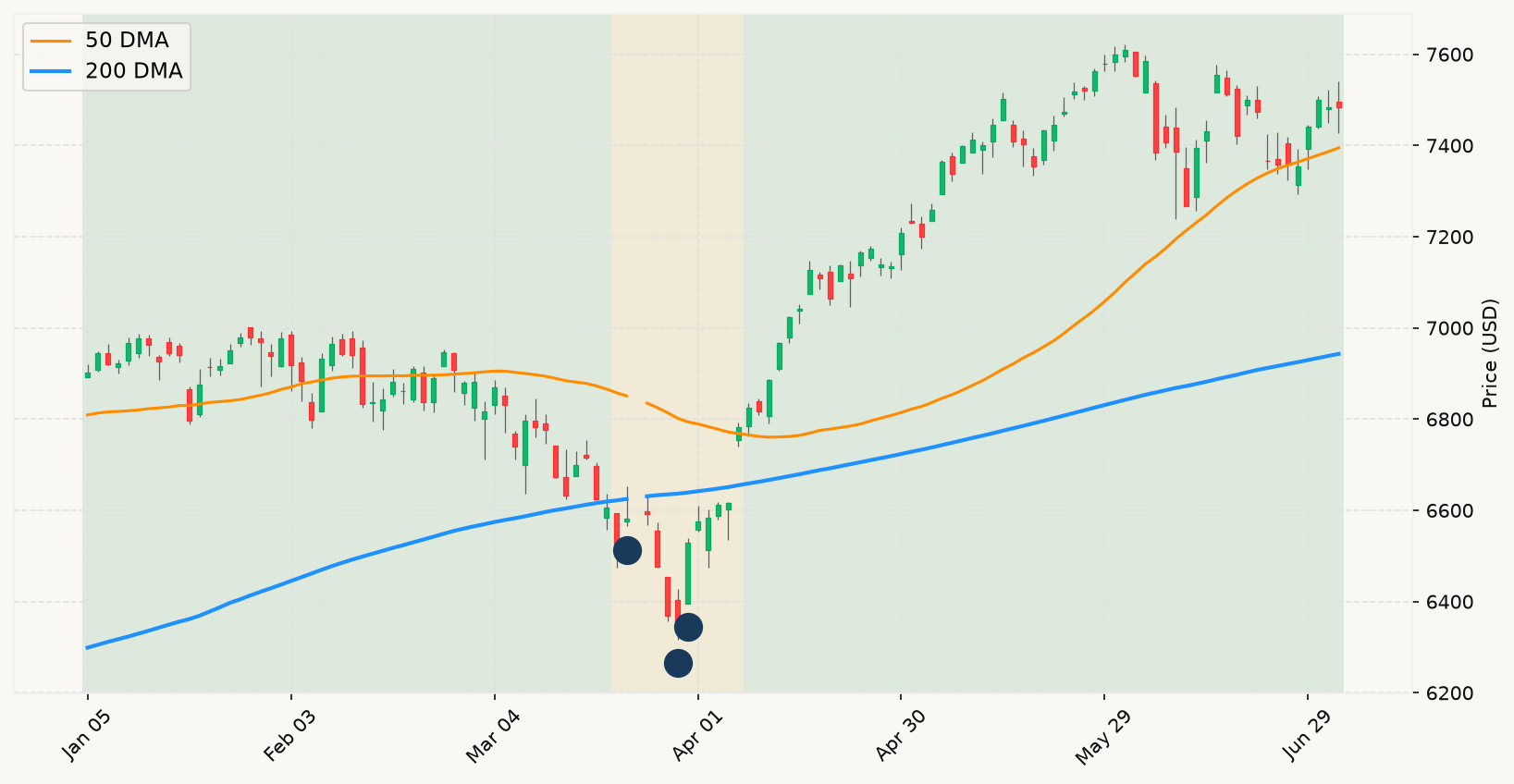

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Noise Everywhere, Signal Nowhere — Stay the Course

The June payrolls miss is classic noise through the lens of what actually matters for long-term investors. A single month's job figure landing below consensus — even by a wide margin — does not move any of the needles that define a regime change. The primary market trend remains firmly bullish; the broad index is well above its long-run trend line, and that is the only technical read that carries diagnostic weight. Everything else is interpretation layered on top of a headline, and the market already digested the number by rallying into a long weekend. The crowd's first instinct — stocks up on softer data — is correct not because of some rate-cut fantasy, but because the data removes an imminent hike risk that had been building into the tape. That's a relief valve, not a fundamental transformation.

The semiconductor selloff deserves the same cool-headed treatment. A sector that roughly doubled in six months correcting 7–10% is not a signal — it is arithmetic. Highly leveraged momentum trades unwind fast and hard when sentiment shifts even slightly, and leveraged ETF rebalancing mechanics can amplify the move well beyond what fundamentals justify. The subsequent bounce in Korean chipmakers and the stabilization in U.S. names confirm what the base rates already suggested: when corrections happen this quickly in high-momentum sectors, the self-correcting mechanism tends to engage just as fast. The underlying AI infrastructure build-out has not been invalidated by a two-day swoon in Micron and Applied Materials. Watch the primary market trend, not the sector volatility.

The oil decline is arguably the most substantive macro development of the week — and it is constructive, not alarming. Energy was the primary transmission mechanism for the 2026 inflation surge, which pushed CPI to a three-year high and forced the Fed into a hawkish posture under Chair Warsh. If U.S.-Iran talks in Qatar produce a durable easing of Strait of Hormuz disruptions and oil settles sustainably in the high $60s, the inflation pressure that has been the dominant constraint on monetary policy softens materially. That improves the interest rate environment without requiring economic weakness. It's the rare macro gift: disinflation arriving through supply restoration rather than demand destruction. The employment conditions data — with labor force participation dropping and payroll gains softening — are consistent with a cooling economy, but not a collapsing one. No leading indicators are converging toward recession; they are simply easing off a hot post-conflict pace.

The composite read across all signals points squarely to the first row of the decision matrix: the market is above its primary trend, the all-time high from June is just weeks away, and the economic signals are mixed-but-not-deteriorating rather than converging on recession. In this regime, the correct posture is fully invested, and the correct response to scary headlines about jobs misses, chip crashes, and geopolitical wobbles is patience. The historical record is clear that 80% of corrections — even significant ones — resolve without becoming prolonged bears, and every one of the four prolonged bears in the modern dataset coincided with an actual recession confirmed across multiple leading indicators simultaneously. None of those conditions are present. Stay invested, ignore the noise, and let the primary trend do its work. MoreLess