The Ticker

Bull Market

The market's throwing a little tantrum in the chip aisle, but the store is still open, the lights are on, and the rest of the shelves are fully stocked — this bull's just catching its breath before the next lap.

Top Story

Chip Stocks Crater as AI Spending Scrutiny Triggers Broad Tech Selloff

The great AI chip trade is hitting a wall. After a dazzling first half that saw semiconductor stocks rack up triple-digit gains, investors are now aggressively questioning whether the returns on all that AI infrastructure spending will ever match the hype — and the selling has been swift and brutal, dragging down some of the market's biggest winners in a single session.

The broader bull market has delivered a stunning first half of 2026, with corporate earnings powering gains across the major indexes even as geopolitical headwinds from the U.S.-Iran conflict rattled nerves. The rotation underway in tech — away from chip makers and toward hyperscalers like Meta, which surged after unveiling plans to monetize its AI computing capacity — suggests the market is beginning to separate AI's winners from its infrastructure overbuilders. That's a maturing narrative, not a collapsing one.

Fed Chair Kevin Warsh, speaking in Sintra, Portugal, delivered a clear message: inflation is still too high and price stability remains the central bank's north star, even as officials grow more open-minded about AI's long-term disinflationary potential. With the June FOMC dot plot already signaling that rate hikes remain on the table for 2026, markets head into Thursday's jobs report acutely sensitive to any data that might tip the Fed's hand — a softer-than-expected ADP print for June added a wrinkle to the labor picture, though nonfarm payrolls remain the real test.

On the geopolitical front, U.S.-Iran peace talks in Doha made what mediators described as "positive progress," and crude oil has continued to slide toward multi-month lows — a development that could gradually ease the energy-driven inflation spike that has kept the Fed sidelined all year. The ceasefire's durability remains uncertain, but easing tensions in the Strait of Hormuz and falling oil prices represent a genuine macro tailwind that the market has not yet fully priced into the Fed's rate path for the second half. MoreLess

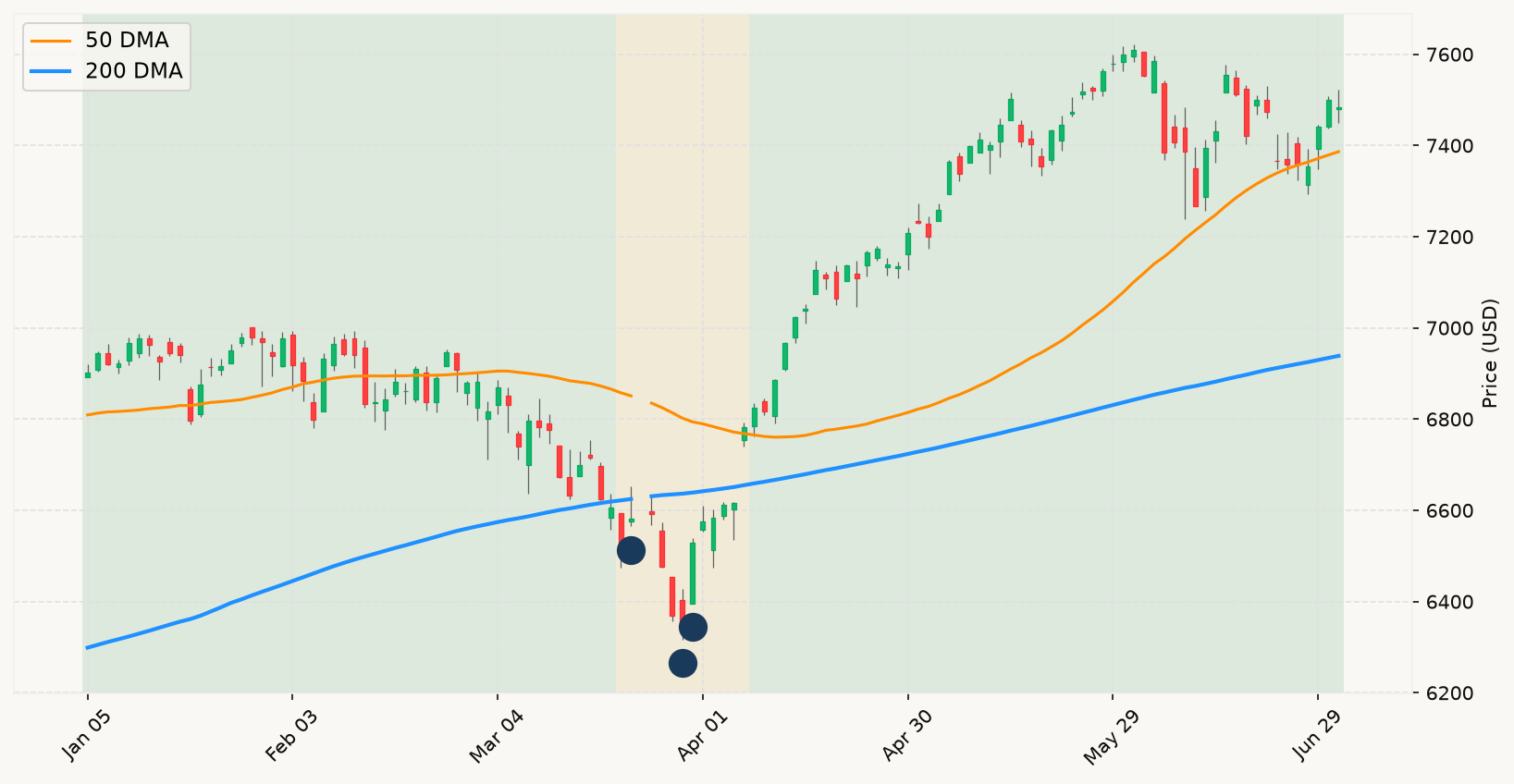

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Market Intact — The Chip Selloff Is a Rotation, Not a Top

The chip selloff is noise — loud, scary-sounding noise, but noise nonetheless. What we saw Wednesday was a sentiment-driven repricing of a sector that had run enormously hard in a short period. Micron, AMD, and Intel didn't suddenly become worse businesses overnight; investors simply decided they'd been priced for perfection and pulled back. The stock market sits comfortably above its primary market trend — a clear bull market regime by any measure — and a 1.7% drawdown from the all-time high does not qualify as a distress signal under any serious analytical framework. The S&P 500 is up nearly 20% year-over-year. This is a healthy market digesting extended valuations in one hot sector, with rotation into hyperscalers like Meta filling the void in real time. That's what bull market corrections look like.

The geopolitical backdrop is incrementally improving, not deteriorating. The Doha talks reporting "positive progress" and crude oil sliding toward multi-month lows are exactly the kinds of developments that could unwind the energy-driven inflation spike that has kept the Fed pinned at 3.5%–3.75% all year. The interest rate environment, while still tilted hawkish, is showing the early signs of a potential pivot in narrative — not in action yet, but in the conditions that would allow action. A sustained decline in energy prices flows directly into headline CPI, and Warsh has been explicit that he will follow the data. If oil cooperates and next month's inflation prints come in softer, the market's current pricing of rate hikes could shift dramatically.

Warsh's Sintra comments — "prices are too high" — are not new information. The market already knows inflation is above target. What matters analytically is whether employment conditions are breaking down in a way that would accelerate recession risk, and the evidence there remains firmly in the green. JOLTS job openings held steady at 7.6 million in May, and even the soft ADP print of 98,000 for June does not signal a labor market in distress. The full nonfarm payrolls report dropping this morning will be closely watched, but the setup heading in — four consecutive months of positive job gains averaging over 100,000 — does not look like the front end of a recessionary contraction. Until employment conditions turn, the second signal required to call a genuine bear market simply isn't there.

The positioning call here is unchanged: stay fully invested. The AI rotation story — from chip infrastructure to monetization plays — is a mid-cycle sector shuffle, not a market top. The hyperscalers that sold off earlier this year are now leading the bounce, Meta's cloud announcement being the clearest example. The bull market's baton is being passed, and strategists at firms like Ned Davis Research are reading this rotation as evidence that "the bull market can continue deep into the second half." Breadth is improving even as semis pull back — exactly the pattern you'd expect from a durable, expanding rally rather than a distribution top. The correct response to this week's headlines is patience, not repositioning. MoreLess