The Ticker

Bull Market

The economy's cooking on all burners, the bulls are doing a victory lap around the track, and the market's got the kind of strut in its step that only comes after a quarter like that — like a team that just won the championship and hasn't yet noticed the new season starting tomorrow.

Top Story

Wall Street Caps Best Quarter Since 2020 as New Tests Loom

Wall Street just closed the books on one of its most impressive three-month stretches in years — a quarter in which fears about a Middle East conflict, sticky inflation, and Fed rate hikes couldn't stop the bulls from charging. Now, on the first day of Q3, investors are taking a breath and asking whether the run still has legs, or whether the record-setting rally borrowed too much from the future.

The earnings story underpinned the entire advance. Estimates for S&P 500 Q2 earnings growth were revised sharply higher over the course of the quarter, driven by an AI-fueled surge in chip stocks that lifted the semiconductor sector to one of its best quarterly performances on record. The Nasdaq gained roughly 21% in the quarter as names like Nvidia, AMD, Intel, and Marvell led the charge, and investors will soon get their first real test of whether those estimates were justified when Q2 reporting season kicks off in July.

On the Fed front, all eyes are on Sintra today, where Chairman Kevin Warsh makes his first major international appearance alongside ECB President Lagarde, Bank of England Governor Bailey, and Bank of Canada Governor Macklem. Warsh has already signaled a hawkish lean — his June press conference prompted markets to begin pricing in a September rate hike — and any reiteration or moderation of that message at the ECB Forum will move markets immediately. The Supreme Court's ruling last week affirming the Fed's independence from presidential removal pressure adds a further layer of institutional clarity, removing one tail risk that had been weighing on long-term rate stability.

The macro backdrop features a few crosscurrents worth watching. Today's ADP report showed June private payrolls at 98,000 — below estimates and the lowest monthly reading in several months — setting up tomorrow's official nonfarm payrolls as the week's defining data point. The Iran ceasefire memorandum signed in mid-June has helped oil prices stabilize below $70, easing the worst-case inflation fears that briefly rattled markets earlier in the conflict. And SpaceX's imminent Nasdaq-100 inclusion next week will unleash billions in passive fund buying, keeping the mega-cap tech spotlight burning well into July. MoreLess

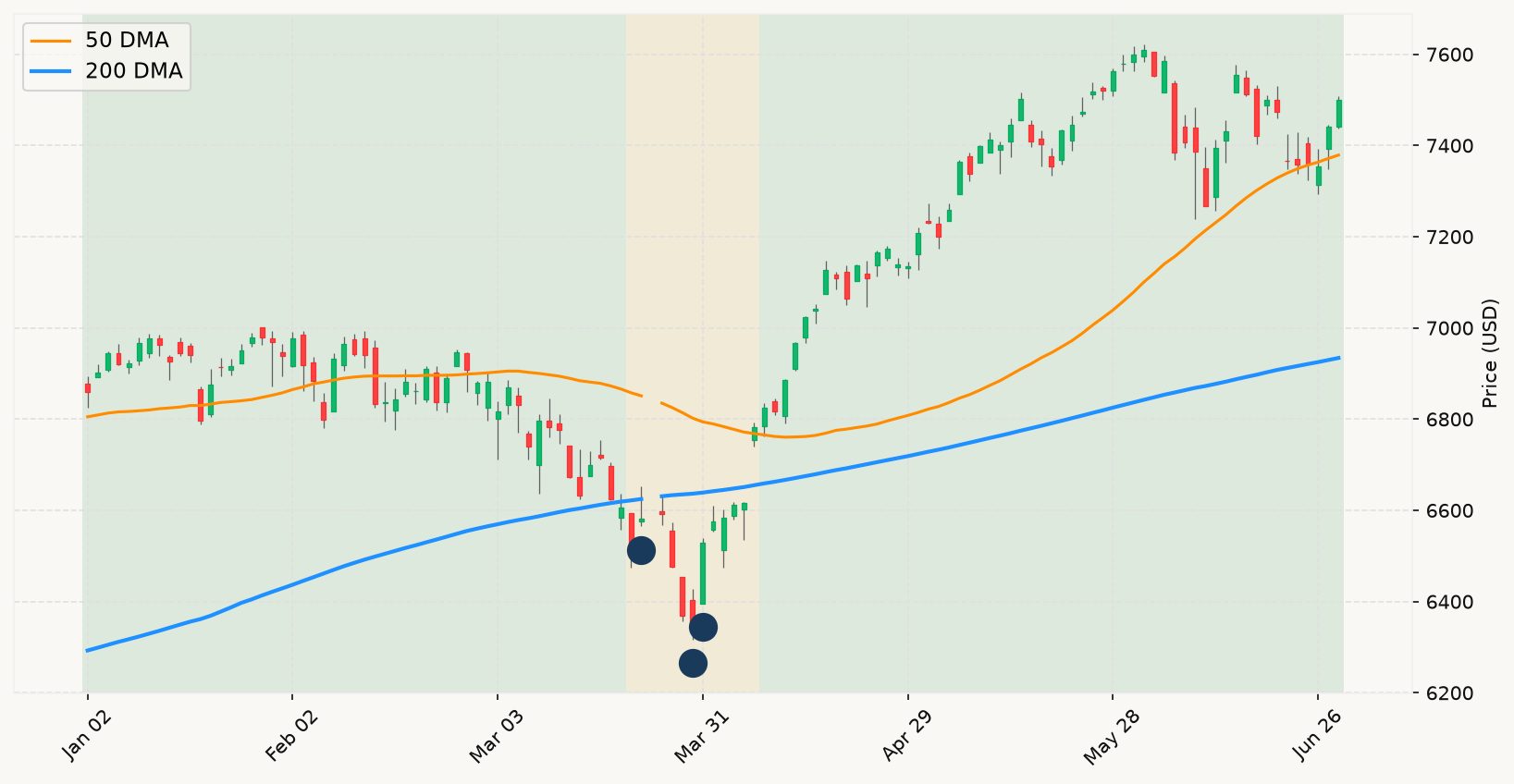

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Market Intact — Stay the Course

The scorecard coming into Q3 couldn't look much cleaner from a trend-following perspective. The primary market trend is firmly bullish, equities just posted one of their best quarters in years, and every major macro signal — employment conditions, the interest rate environment, and growth nowcasts — remains constructive. The drawdown from the June all-time high is trivial, well under 2%, and the velocity of that pullback bears zero resemblance to the slow, grinding profile that historically precedes a recessionary bear. This is textbook bull market noise, not a diagnostic event requiring any defensive response.

The ADP miss and the Warsh Sintra appearance are generating the most headline anxiety today, and that anxiety is, frankly, noise in the strictest sense. Yes, June private payrolls at 98,000 came in light, but a single month's ADP print — with its well-documented divergence from the official Bureau of Labor Statistics report — carries no weight as a recession signal. Employment conditions remain broadly healthy; the Sahm-equivalent labor market signals show nothing resembling the deterioration that would trigger the second leg of a bear market diagnostic. Tomorrow's official nonfarm payrolls report is the one worth watching, and even a modest miss there doesn't move the needle materially.

Warsh at Sintra is a genuine market-mover for rates expectations in the short run, but it's worth being precise about what that means for equity positioning. The hawkish rate environment has already been priced into the interest rate environment over the past several months. The Supreme Court's ruling reinforcing Fed independence is actually a net positive for long-term rate stability — it reduces the tail risk of politically-pressured rate cuts that could reignite inflation and force a more severe tightening cycle later. An independent Fed fighting inflation credibly is a better backdrop for equities than a politically captured one running loose policy. The ruling was a green light for the bond market's confidence in the Fed's institutional credibility.

SpaceX entering the Nasdaq-100 next week and the wrap-up of the best quarterly performance since 2020 are both signals pointing in the same direction: the primary uptrend is intact, momentum is positive, and the AI-driven capex cycle that powered this quarter's chip-stock surge hasn't broken. The 80/20 base rate says that in the absence of converging recession signals, the overwhelming historical probability is that we're in a self-sustaining bull market, not the early innings of something darker. The posture remains fully invested. Wait for real signals — a sustained break of the primary trend line, or meaningful deterioration across multiple leading economic indicators simultaneously — before entertaining any defensive repositioning. Neither condition is present today. MoreLess