The Ticker Analysis

Bull Trend Intact — Stay Invested & Tune Out the Noise

The Supreme Court's decision to shield Fed Governor Lisa Cook from removal is exactly the kind of news the framework classifies as signal-adjacent but ultimately noise for the primary trend. Here's the distinction: the ruling removes a tail risk — the possibility that the White House could install a politically compliant Fed and force premature rate cuts or hold, distorting the interest rate environment in ways that create misallocations. That tail risk had been quietly embedded in risk premiums, particularly in financials and rate-sensitive sectors. Its removal is genuinely constructive. But the market is already comfortably above its primary trend line — the stock market trend remains firmly bullish — and there is no recession confirmation anywhere on the horizon. The ruling is a headwind removed, not a new catalyst created. The correct posture doesn't change: stay fully invested.

The geopolitical picture around Iran-U.S. tensions is pure noise by the framework's standards, and the market's behavior Monday proved the point. Last week's tech selloff, partially attributed to Middle East anxiety, reversed almost entirely in a single session once the ceasefire framework held. This is the velocity diagnostic in miniature — fast, sharp, sentiment-driven moves that resolve quickly. The VIX flirting with 20 last week and retreating this week is the market telling you exactly what the data says: this was not a fundamental repricing event. Investors who panicked out of tech positions during last week's five-session Nasdaq losing streak woke up Monday having missed a 2%+ recovery. That is precisely the cost of reacting to headlines rather than reading the primary trend.

The Comcast spinoff and Rocket Lab-Iridium deal are interesting corporate stories, but the framework's lens on them is straightforward: large, long-duration M&A activity is a lagging sentiment indicator, not a leading one. Boards approve $8 billion acquisitions and multi-billion-dollar corporate restructurings when they are confident about the macro backdrop. That confidence is consistent with everything else the market is telling us — employment conditions remain healthy, monetary policy signals are constructive with the curve in positive territory, and real GDP growth nowcasts are solidly positive. Neither deal is a signal about market direction. They are evidence of animal spirits operating in a bull market environment, which is exactly where we are.

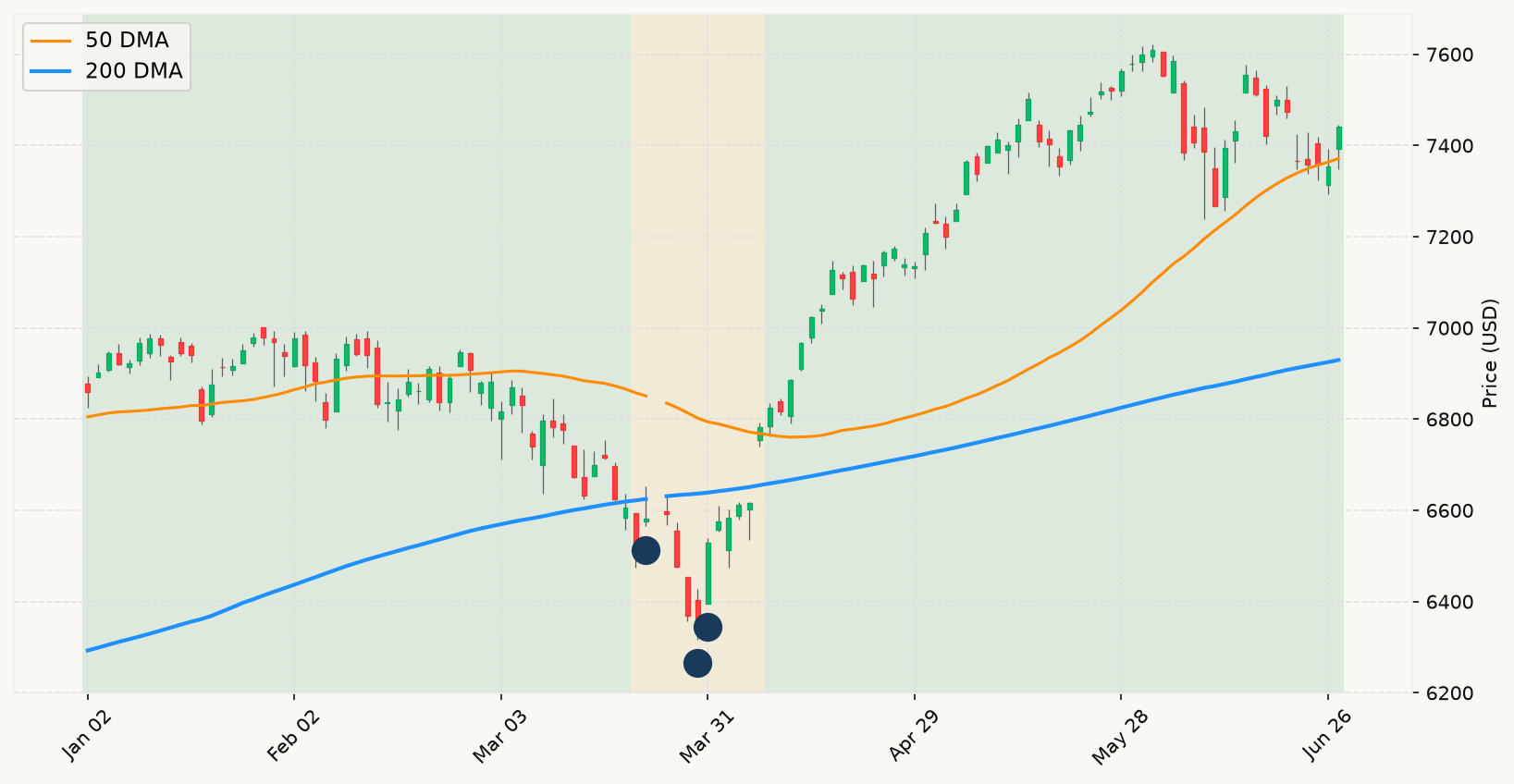

The week's real market-moving event is Thursday's June nonfarm payrolls report — the first hard labor market data of the second half of 2026. Consensus around 110,000 represents a meaningful step down from May's 172,000, and that deceleration is worth watching not because a single print triggers anything in the framework, but because the labor market is one of the four leading indicators that would need to deteriorate in concert with a grinding equity decline to raise the recession flag. Right now, employment conditions are firmly in the bullish column. A print at or above 100,000 changes nothing. A significant miss combined with upward revisions to unemployment would be the first data point worth monitoring — not reacting to, monitoring. The base rate remains overwhelming: the market is above its primary trend, the economy is growing, and 80% of 10%+ corrections in the historical record resolved without becoming prolonged bear markets. There is no 10% correction to speak of right now. The correct posture is to enjoy the ride. MoreLess