The Ticker Analysis

Bulls in Charge, Bears Lack the Evidence

The dominant headline today — Iran peace talks resuming in Doha despite a weekend of renewed drone strikes — is squarely in the "noise" category from an analytical standpoint, and that verdict holds even though it sounds alarming. The market already digested the full shock of the Iran war beginning in late February, the Strait of Hormuz closure, and the energy price spike that pushed PCE to a three-year high. The S&P 500 not only absorbed all of that but went on to set a new all-time high on June 2. A market that can make new all-time highs through an active shooting war involving major oil infrastructure is not a market signaling recessionary distress. The geopolitical calendar — today's Doha meeting, the fragile ceasefire, the ongoing nuclear talks — is background noise. The market has already voted on it with its feet.

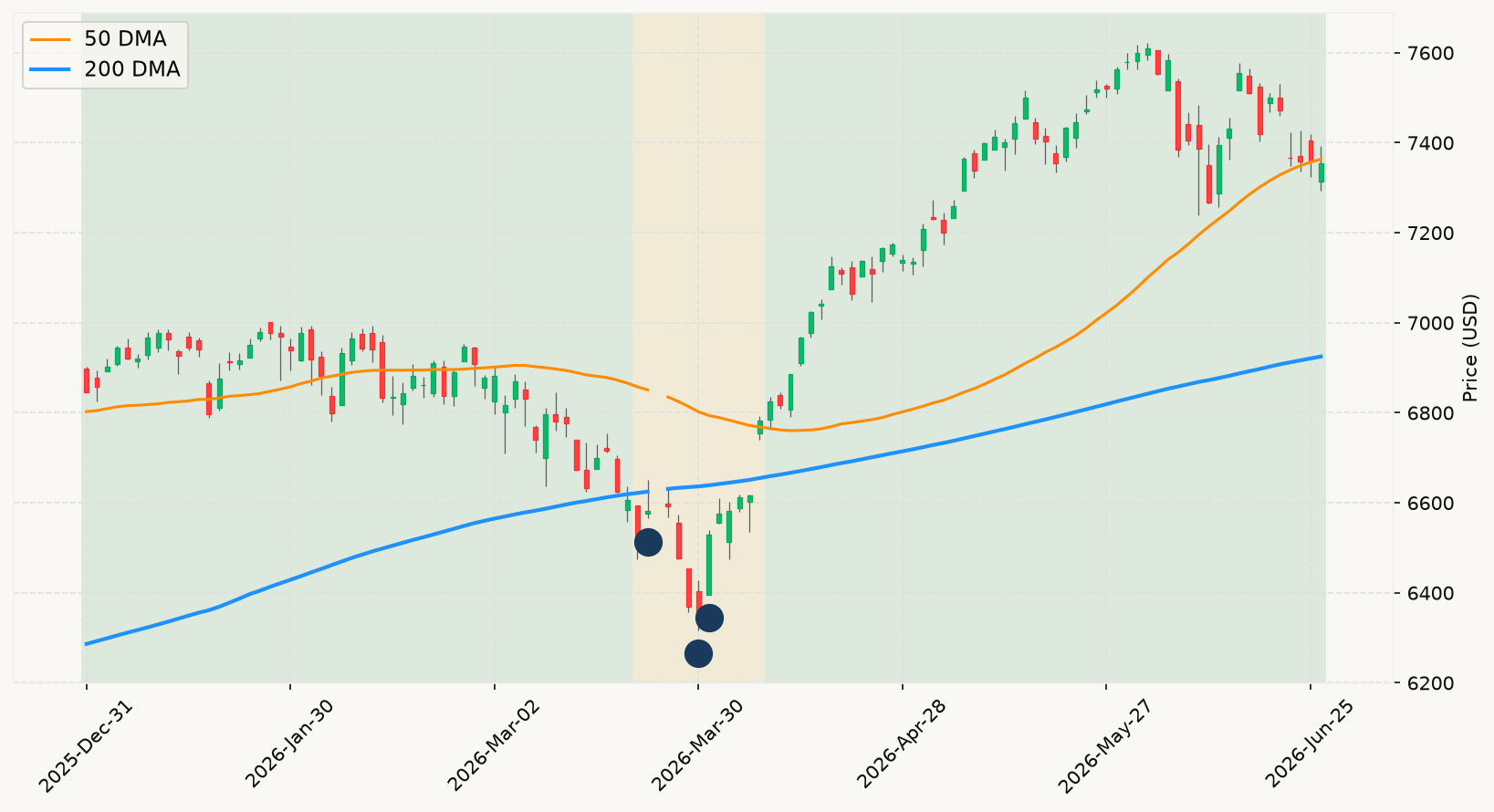

The primary stock market trend is unambiguously bullish. The index is sitting well above its long-term trend line, the all-time high is only four weeks old, and the current pullback from that high is modest. Nothing about the velocity or magnitude of this drawdown suggests a gradual, grinding recessionary decline in early formation. The rotation we're seeing — out of mega-cap tech, into healthcare, industrials, and small caps — is actually a breadth improvement, not a deterioration. When the equal-weight index outperforms the cap-weighted headline by 350 basis points in a single week, that's the market getting healthier, not sicker. Broad participation is the hallmark of a durable bull, not a warning sign.

The most legitimate near-term concern is on the inflation and Fed policy side. PCE at a three-year high, with the FOMC explicitly leaving the door open to a September hike, represents a genuine tightening of the interest rate environment. But context matters: the same PCE report showed consumer spending and personal income both running hot, well above expectations. That is not the combination you see at the onset of a recessionary contraction. Both real-time growth trackers are solidly positive. Employment conditions remain strong — initial claims are low and falling, and the Sahm Rule analog shows no deterioration. For the recession signal to become actionable, you need the labor market to crack and the real-time growth signals to turn negative. Neither is happening. A Fed rate hike in September would be a headwind, not a death knell.

The OpenAI IPO delay and the SpaceX post-IPO selloff are pure noise from a portfolio posture standpoint. The history of high-profile IPOs underperforming in their first year is well-documented, and sentiment-driven repricing of individually hyped names does not move the framework's recession indicators by a single basis point. Investors who own diversified index funds are already appropriately positioned — they own every winner in this market, including whatever AI infrastructure spending cycle ultimately generates value, without having to bet on which company captures it. The correct posture here remains fully invested. The burden of proof for a defensive shift falls entirely on the bear case, and the bear case currently lacks both required legs: neither a sustained breach of the primary market trend nor a convergence of deteriorating economic signals is present. MoreLess