The Ticker

Bull Market

The economy's engine is purring like a well-fed cat — a few bumps in the road from overseas, prices nudging higher at the checkout, but the sun is still shining and the picnic isn't going anywhere.

Top Story

AI Memory Crunch Forces Apple & Microsoft to Hike Prices

The AI buildout has officially landed in your shopping cart. Apple raised prices on MacBooks and iPads by as much as 25%, while Microsoft announced Xbox console hikes of up to $150 — both companies pointing the finger at a semiconductor market under extraordinary strain as data center operators vacuum up memory chips faster than manufacturers can produce them. For ordinary consumers, it's the clearest sign yet that the AI boom has real-world, real-dollar consequences.

This week's earnings season coda delivered a split verdict. Micron Technology's blowout quarterly results — record revenue and a bullish forward outlook — validated the AI memory thesis for chip suppliers but paradoxically hammered the stocks of the tech giants being squeezed by the same chip costs. With July earnings season restarting shortly, the bar is now high: analysts have been ratcheting up expectations for AI-exposed names, and any sign of margin compression from memory costs will be closely scrutinized.

The Federal Reserve finds itself in a tough spot. May PCE inflation came in at a three-year high, and new Fed Chair Kevin Warsh has been unambiguous about his commitment to price stability — dropping a previously-indicated rate cut and leaving the door open to a hike as early as September. The memory chip inflation feeding into consumer hardware prices is exactly the kind of cost-push pressure that complicates the Fed's calculus, since it isn't easily addressed by tightening demand.

Beyond the chip story, two macro wildcards are keeping traders on edge. Iran's drone strike on a Singapore-flagged cargo vessel in the Strait of Hormuz — the first attack since last week's U.S.-Iran ceasefire agreement — rattled oil markets and briefly spiked crude prices, casting doubt on whether the critical shipping corridor will stay open. And Volkswagen's reported plan to eliminate up to 100,000 jobs and shutter four German plants underscores how profoundly the AI economy is reshaping global industry, squeezing legacy manufacturers caught between an expensive EV transition and relentless Chinese competition. MoreLess

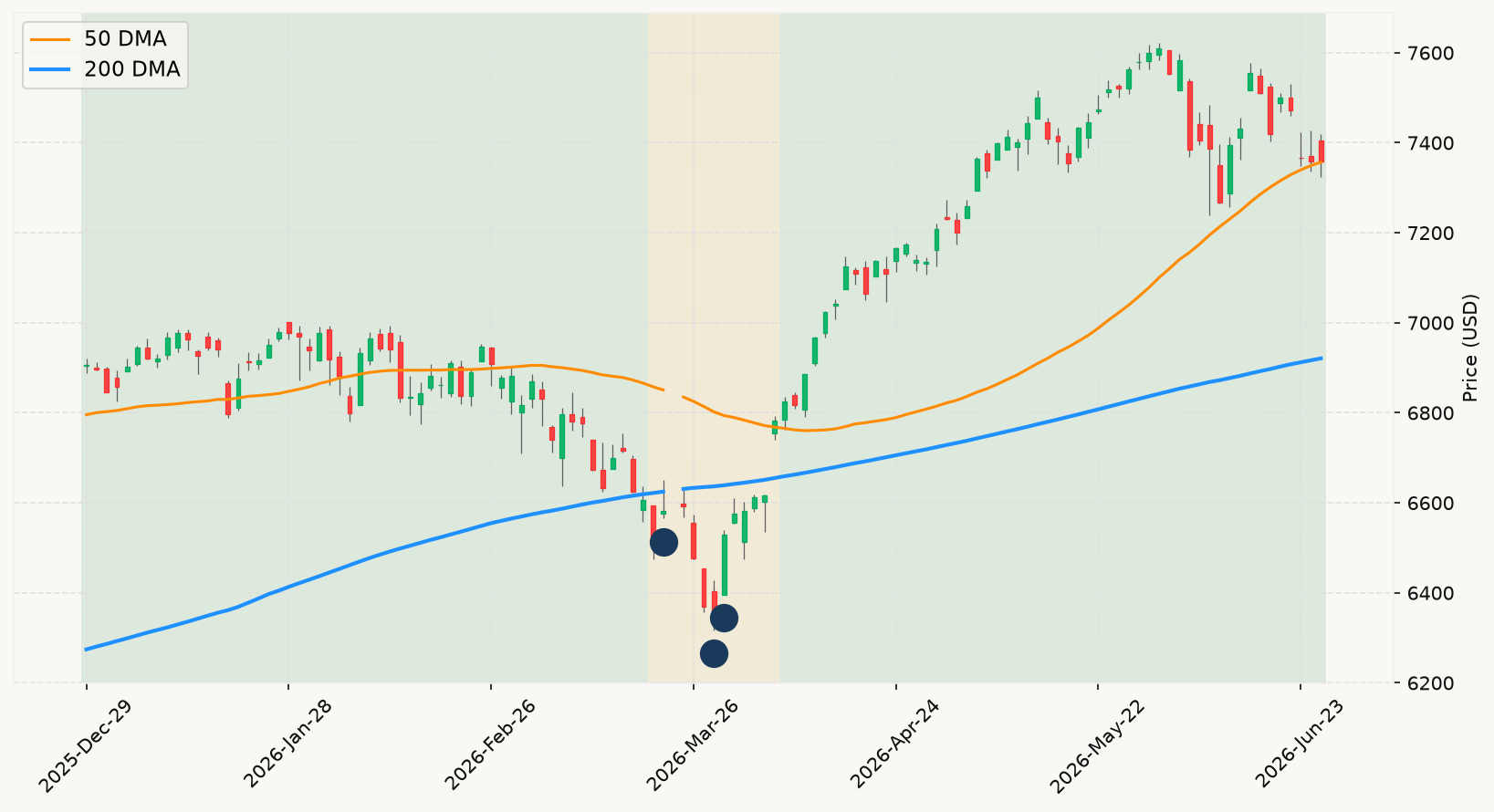

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Case Intact — This Dip Is Just Noise

The market's current setup checks every box for the bull case: the primary market trend is intact and firmly bullish, the interest rate environment shows no inversion, labor markets remain healthy, and the nowcasting data points to solid Q2 growth. Against that backdrop, this week's turbulence in megacap technology — driven by Apple's hardware price hikes, mounting anxiety about AI spending discipline, and a Nasdaq that strung together four consecutive losing sessions — is precisely the kind of noise the data says to ignore. The market pulled back roughly 3% from its June 2 all-time high. That is not a signal. That is a routine shakeout of crowded positioning in a sector that was up nearly 30% in three months. The framework's default posture in this environment is unambiguous: stay fully invested.

The Apple and Microsoft price hike story is genuinely important news — but not for the reason the headlines imply. It does not change the primary market trend. It does not move any leading economic indicator toward recession confirmation. What it does do is confirm that the AI buildout is real, capital-intensive, and reaching into every corner of the economy. Micron's blowout earnings are the other side of that same coin: the companies supplying the memory chips powering AI infrastructure are minting record profits. Investors rotating out of megacap consumer-facing tech and into semiconductor suppliers are following the money correctly, even if the index-level read looks like a sell-off. Broad index holders own both sides of that trade automatically.

The PCE print and the Fed's hawkish pivot under Kevin Warsh deserve attention, but not alarm. Elevated inflation driven substantially by an energy shock and AI-induced component cost inflation is the kind of supply-side pressure that the Fed can acknowledge without necessarily triggering the sustained demand destruction that precedes a recessionary bear. The interest rate environment remains positive — no inversion signal, the spread is firmly in positive territory — and both GDP nowcasts are tracking well above zero. The Fed may hike in September; that is not the same as the economy tipping into contraction. Rate hikes into a strong labor market with solid growth are a tightening of conditions, not a recessionary event in themselves. Four of the last five rate-hike cycles ended without a recession. The convergence test — where multiple leading indicators simultaneously deteriorate and a grinding market decline confirms — is nowhere close to being met.

The Strait of Hormuz attack and the Volkswagen restructuring are both legitimate geopolitical and industrial stories, but neither clears the bar to become a market signal under any sensible analytical framework. The shipping disruption risk has been embedded in oil prices and inflation expectations for months; one additional drone strike does not change the probabilistic picture in a direction the market hasn't already priced. Volkswagen shedding jobs is a company-specific response to competitive pressure from Chinese automakers and an expensive EV transition — a European industrial story, not a leading indicator of U.S. recession. The market has already moved the primary trend indicator far above the levels that would raise a bear market alert. Until that changes — or until labor market, growth, and credit signals converge in a deteriorating direction — the historically correct posture is the same one it has been all year: own the broad market, do nothing, and let the compounding work. MoreLess