The Ticker

Bull Market

The bulls are charging like it's a rodeo Friday — AI money is gushing, chips are sizzling, and the whole barnyard is feeling fine.

Top Story

Micron's Blowout AI Earnings Ignite the Chip Trade & Lift Markets

Micron Technology just delivered one of the most impressive earnings results in semiconductor history, sending its stock soaring more than 15% in after-hours trading and lighting a fire under the broader market heading into Thursday. The memory chip giant blew past Wall Street's already-lofty expectations on both revenue and margins, with management offering guidance that was even more bullish — a powerful signal that the AI infrastructure buildout is still running at full throttle.

The earnings season backdrop matters here. Micron's report served as a capstone to what analysts described as a stunning run of corporate results. The company posted earnings per share of $25.11, smashing estimates of $20.20 by nearly 25%, and reported gross margins of 84.9% — the highest in company history. With Micron's entire 2026 high-bandwidth memory output already contracted under take-or-pay agreements with data-center customers, the report validated the view that AI capital spending is not slowing, it's accelerating.

The Federal Reserve is the other major variable hanging over every market move right now. New Chair Kevin Warsh held rates steady at 3.50%–3.75% at the June FOMC meeting, but the dot plot showed nine officials projecting at least one rate hike by year-end, and the Fed revised its PCE inflation forecast sharply higher. Markets have now priced out rate cuts almost entirely for 2026 — putting the focus squarely on this morning's May PCE report as a potential catalyst for repricing in either direction.

On the macro front, the economy continues to expand at a solid pace even as the interest rate environment remains elevated and restrictive. Real GDP grew 1.6% annualized in Q1, and real-time growth trackers point to a meaningful pickup in Q2. The SpaceX IPO drama — now compounded by a $25 billion debt offering that strained the newly minted stock — and Alphabet's impending addition to the Dow are additional storylines reflecting just how much the market's center of gravity has shifted toward mega-cap technology and AI infrastructure. MoreLess

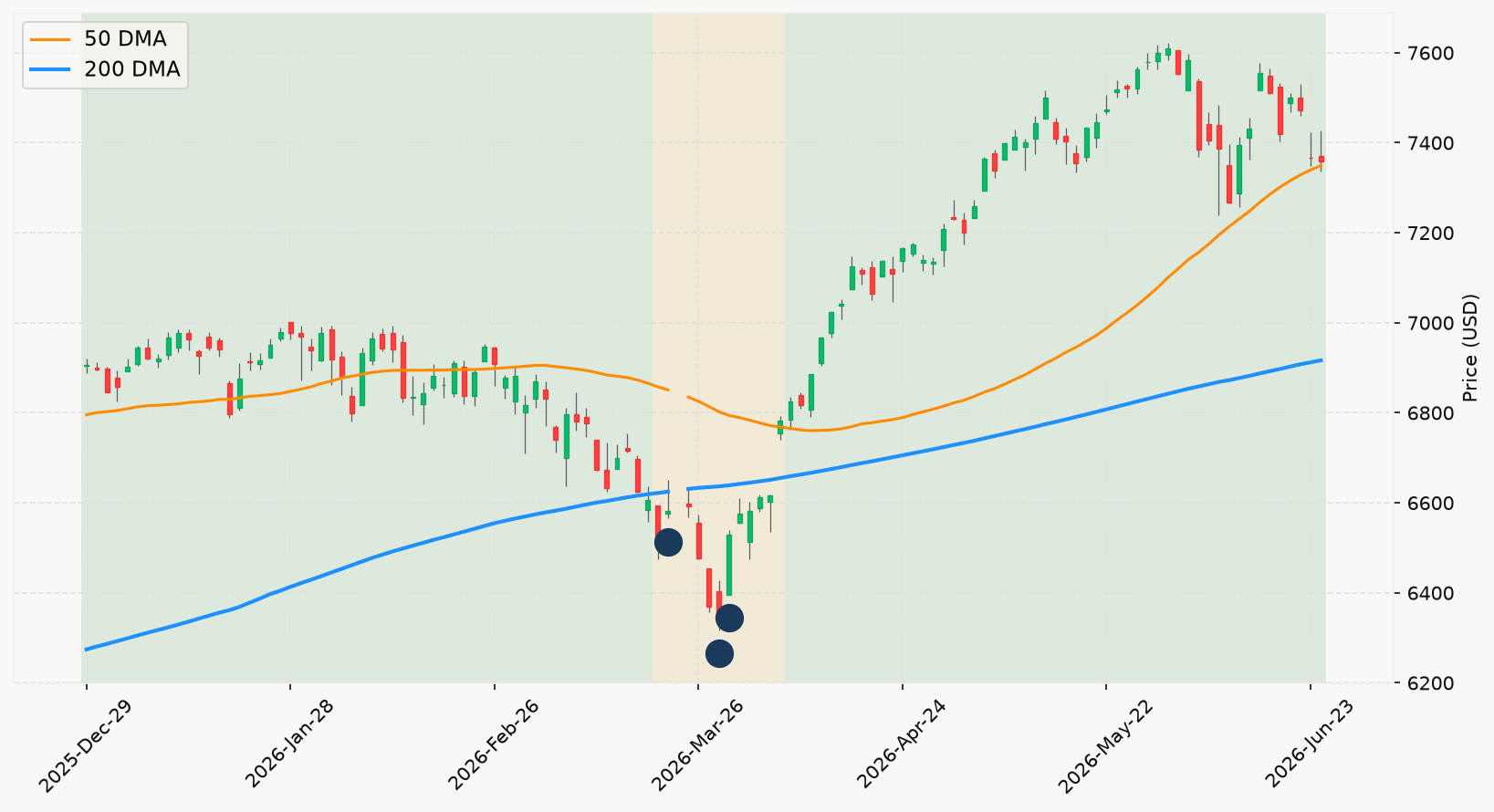

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Market Intact — Micron Is Noise, Not Signal

The Micron blowout is exactly the kind of number that dominates financial media and feels like a critical signal — but applying rigorous thinking, it belongs firmly in the noise bucket. Earnings reports, however spectacular, are lagging information: by the time a company reports, the result is already baked into prices. The market had already given Micron a massive run, hitting an all-time high earlier in the week. What matters for the investment posture is not what Micron just earned, but what the primary market trend and economic indicators are telling us. And right now, they are telling a clear story: the market is solidly above its long-term trend line, the economic expansion is intact, and this is not a moment to be hunting for exits.

The monetary policy environment is the most interesting moving part right now. New Fed Chair Kevin Warsh's first FOMC meeting produced a hawkish surprise — a dot plot with nine officials penciling in at least one hike, a PCE inflation forecast revised sharply higher, and forward guidance that was conspicuously absent. Markets have repriced accordingly, with rate cuts now effectively off the table for 2026. The interest rate environment is clearly more restrictive than it was six months ago. But here's what the historical record shows: a restrictive but positive-sloped rate environment — where short rates are rising but the spread between long and short rates remains positive — is not the same as the inversion signal that has historically preceded recessions. The 10-year/3-month spread remains comfortably positive. There is no inversion. No recession signal here.

The SpaceX debt drama and the Dow reshuffle are textbook noise. A high-profile IPO stock trading erratically in its first weeks of public life tells you nothing about the health of the broader equity market. Index rebalancing events like the Alphabet/Verizon swap generate short-term mechanical buying and selling pressure but carry no informational content about where the economy is heading. The real read on the macro is in the growth trackers: both real-time GDP models are firmly positive, employment conditions remain strong with no deterioration that meets the historical threshold that has preceded recessions, and the market itself — the most comprehensive aggregator of all available information — remains well above its long-term trend. All four of the key recession signals are green or neutral.

Bottom line: the current regime is a bull market with elevated but non-recessionary inflation and a watchful Fed. The modest pullback from the early June all-time high is entirely consistent with normal intra-year volatility — statistically, a pullback in this range happens virtually every year and resolves without incident roughly 80% of the time even when it gets larger. The velocity of any decline so far is nowhere near the gradual, grinding profile that has historically characterized the early stages of a recessionary bear. Stay fully invested. Today's PCE print could create intraday noise in either direction, but it is not a reason to change posture. The framework is not triggered. MoreLess