The Ticker

Bull Market

The economy's humming like a well-tuned engine, the geopolitical storm clouds are parting over the Persian Gulf, and even with the chip sector throwing a little tantrum, the overall market barnyard is full of contented bulls grazing in sunshine.

Top Story

Micron's Monster Earnings Report Is the AI Trade's Biggest Test Yet

All eyes on Wall Street are locked on Micron Technology tonight as the memory chipmaker delivers what could be the defining earnings report of the AI boom. Analysts are expecting a near-1,000% surge in year-over-year profits, fueled entirely by the AI industry's voracious appetite for high-bandwidth memory — the specialized chips that power data centers and large language models. With Micron shares already up hundreds of percent in 2026, the stakes for the after-hours print could not be higher.

The broader earnings season context is extraordinary. Nvidia and Micron have together become the twin engines of tech-sector profit growth, and Micron's HBM capacity is reportedly sold out through the end of 2026. That supply constraint has handed the company exceptional pricing power, helping push gross margins from the mid-30% range a year ago to north of 75% last quarter. Tonight's Q4 guidance — particularly any update on HBM allocation and DRAM pricing — will do more to set the near-term tone for semiconductor stocks than the headline EPS figure alone.

On the Fed front, the FOMC held rates steady at its June 16–17 meeting, but markets are increasingly pricing in the possibility of at least one hike before year-end. The June dot plot nudged the median year-end fed funds projection a quarter-point higher, and the dollar's run to new 2026 highs this week reflects that repricing. The Fed's June statement acknowledged that inflation "remains elevated relative to the Committee's 2 percent goal," pointing in part to supply shocks from energy and geopolitical disruptions — the same forces now easing with the U.S.-Iran peace framework.

That peace framework is a genuine macro wildcard. The interim U.S.-Iran deal — signed at Versailles — reopens the Strait of Hormuz toll-free for 60 days, and crude oil has cratered back toward pre-conflict levels as a result. The disinflationary tailwind from falling energy prices is real, but the deal remains fragile: Iran insists on "service fees" after the 60-day window, and unresolved nuclear and Lebanon questions leave the situation in flux. Treasury Secretary Bessent's bullish call for 3% GDP growth this year rests heavily on whether this détente holds. MoreLess

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Trend Holds — Chip Chaos Is Just Noise

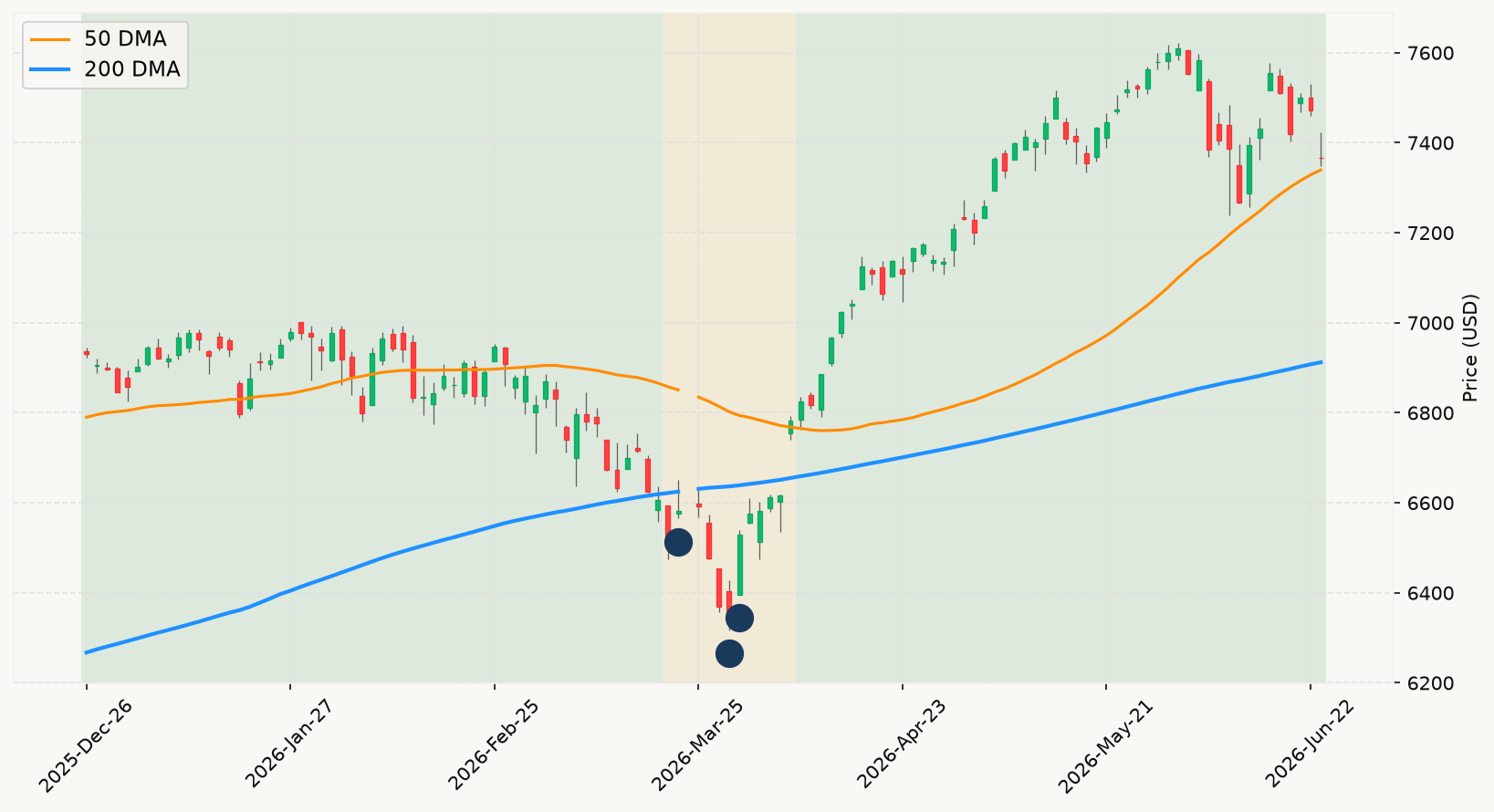

The market is above its primary trend line — squarely in bull market territory — and tonight's Micron print is a perfect illustration of why the framework treats news events as noise rather than signal. Micron's earnings are expected to be spectacular, and the stock is down sharply from recent highs on AI sector rotation fears. None of that changes the signal. The market is above its long-term trend. The economic nowcasts are solidly positive. Employment conditions show no deterioration. The interest rate environment, while tighter than a year ago, is not flashing recession warning signals — the 10-year/3-month spread is in positive territory, the exact opposite of the configuration that has preceded every modern U.S. recession. The diagnostic is clean: this is a bull market experiencing a tech sector air pocket, and that is not a reason to reposition defensively.

The semiconductor volatility is worth addressing directly — because it feels significant even if it isn't. A 13% single-day drop in a high-flying chip name, followed by a global ripple through Asian and European markets, is precisely the kind of dramatic event that makes investors question whether something bigger is breaking. It isn't. What the framework looks for is a gradual, grinding decline in the broad market accompanied by converging deterioration in leading economic indicators. What we have instead is a sharp, fast selloff concentrated in a crowded leadership sector — the signature of a sentiment correction, not systemic repricing. The S&P's drawdown from its all-time high remains modest. History is unambiguous: fast, steep declines in narrow sectors that do not spread to the broad economic backdrop resolve. Staying put is the evidence-based response.

The U.S.-Iran peace framework and the reopening of the Strait of Hormuz are genuinely significant macro developments — but not for the reasons market commentators will emphasize today. The disinflationary impulse from collapsing crude prices matters for the Fed's next move. The June dot plot already pointed toward a possible hike before year-end, and a sharper-than-expected drop in energy prices could flip that calculus toward a hold or even a cut. That dynamic — a Fed that finds itself with more room to maneuver as geopolitical energy risk fades — is structurally supportive for equities. It reinforces the bull case without changing any of the framework signals. The market trend is bullish. Economic momentum is positive. The setup remains fully invested.

The dollar's move to 2026 highs and the market's repricing of Fed rate expectations deserve a measured read. Rising rate hike odds have historically been a headwind for growth and tech multiples — but the framework doesn't trade on rate speculation. It watches what the market actually does. A broad market that holds its trend line in the face of rising rate expectations and semiconductor turbulence is a market demonstrating resilience, not fragility. Until the primary trend breaks and economic indicators begin converging toward contraction, all of this qualifies as noise — including the Micron drama, the oil probe, and the geopolitical fog around the Iran deal. The base rate says 80% of corrections resolve without becoming prolonged bears. Nothing on the board today moves that needle. MoreLess