The Ticker Analysis

Bull Trend Intact: Today's Drama Is Just Noise

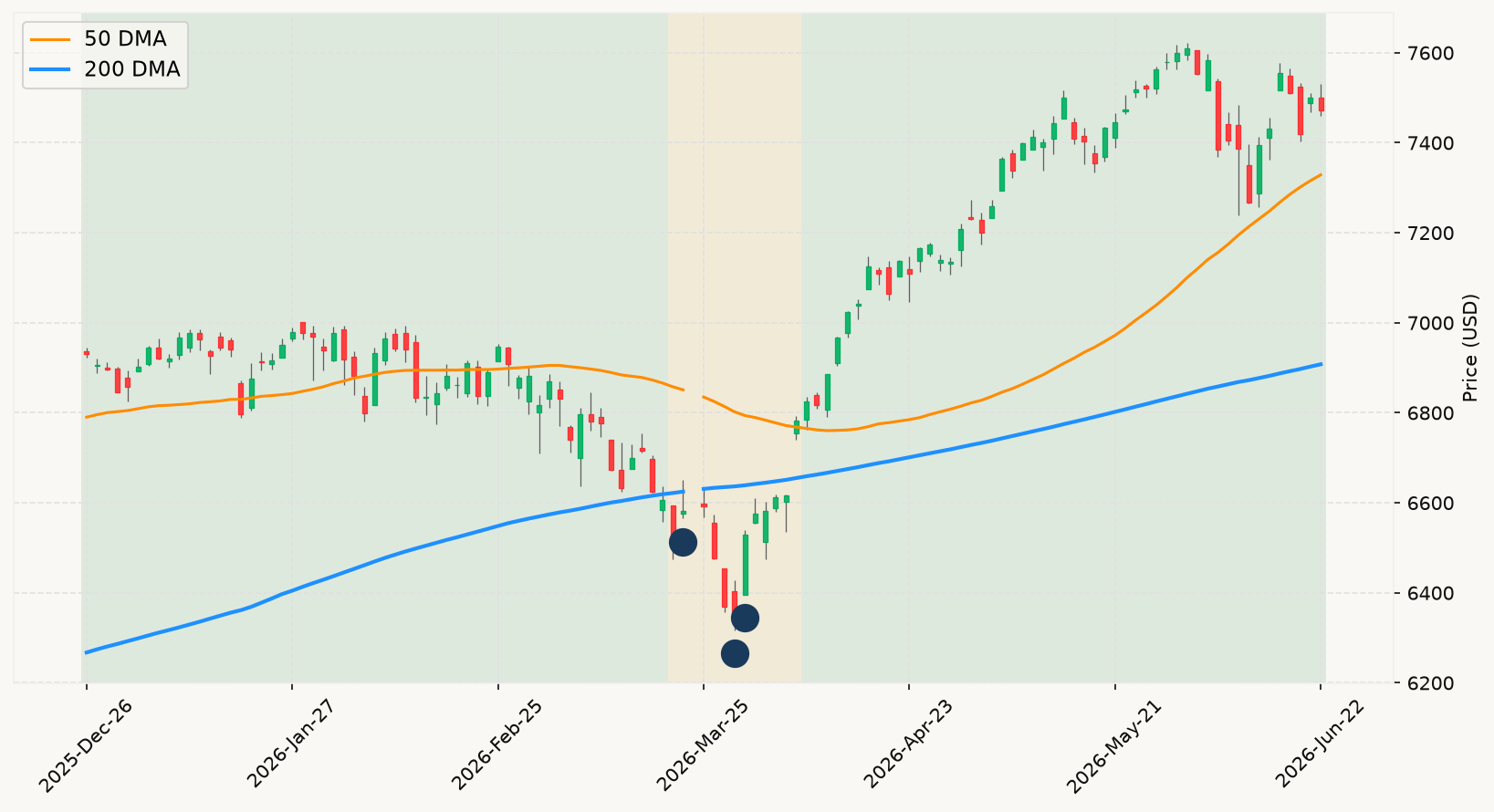

The headline today is a global tech rotation triggered by South Korea's chip meltdown, with AI names selling off hard across time zones and U.S. futures pointing to a red open. Investors conditioned by months of one-directional momentum are understandably rattled, but the analytical read here is clear: this is noise, not signal. The S&P 500 remains solidly above its primary market trend, sitting nearly 8% clear of that long-run benchmark. A rotation out of crowded trades — particularly into the hyper-concentrated semiconductor and mega-cap AI complex — is not a recession. It's a rebalancing. The velocity and profile of this pullback, barely 2% from the all-time high with no grinding deterioration, maps precisely to the corrective episodes that resolve quickly. There is no evidence here that the broad market's uptrend is threatened.

The more consequential development this week is the Fed's hawkish pivot under Chair Warsh. Nine of 18 FOMC participants are now penciling in at least one rate hike for 2026 — a sharp reversal from a posture that was leaning toward cuts just a few months ago. This matters for the interest rate environment, but it needs to be assessed correctly. The primary market trend remains bullish. A rate hike in isolation, without a corresponding deterioration in labor market conditions or a genuine turn in the growth nowcasts, is not a recession trigger. The economy is currently running at a solid pace by real-time estimates from both major nowcasting models. Employment conditions remain healthy by every leading measure available. A hawkish Fed that hikes into a resilient economy is a very different animal from a Fed hiking into a deteriorating one — and historically, the former has not derailed bull markets. The correct posture remains fully invested.

Oracle's disclosure that AI directly eliminated 21,000 jobs is a legitimate macro conversation starter, but again the framework is clear on this: corporate restructuring announcements, however significant in scale, carry no predictive weight for near-term market direction. The same is true of SpaceX's post-IPO meltdown — a textbook case of sentiment-driven froth correcting after an extended squeeze in a thinly floated new issue. Neither the Oracle layoff disclosure nor the SpaceX reversal moves any needle in the leading indicator constellation that actually matters. Both are noise. What they collectively underscore is that the AI capital allocation cycle is entering a more demanding phase where markets will scrutinize monetization far more closely — but that scrutiny plays out over quarters and earnings cycles, not in the kind of grinding, confirming deterioration that precedes a prolonged bear.

The UK political transition, with Starmer out and Burnham poised to take Number 10, adds headline drama but is a third-tier input for U.S. equity investors. Global geopolitical friction — including ongoing U.S.-Iran negotiations and Hormuz uncertainty — is already reflected in the interest rate environment and commodity prices. None of this represents a convergence of the kind that has historically preceded true recessionary bear markets. The posture today is unchanged: stay fully invested, treat today's volatility as the cost of equity ownership rather than a warning signal, and resist the pull of headlines that feel urgent but carry no diagnostic weight. The market remains in a bull trend until the data says otherwise — and right now, the data doesn't say otherwise. MoreLess