The Ticker Analysis

Bull Market Intact — Noise, Not Signal

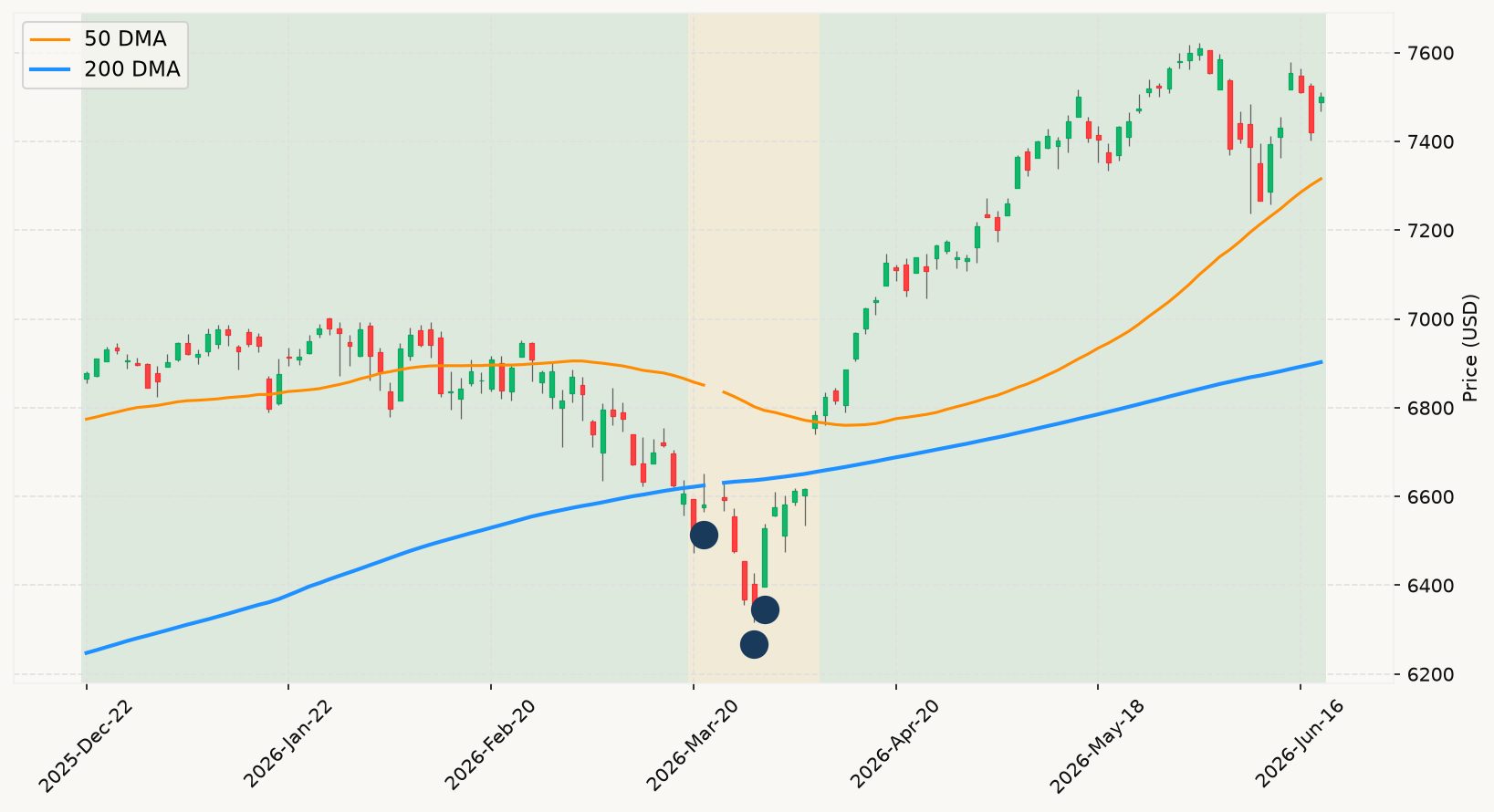

The primary market trend is unambiguous: equities are trading comfortably above their long-term stock market trend, the S&P 500 just wrapped its 11th winning week in 12, and the index sits only about 1.4% below its all-time high set barely two weeks ago. That configuration — price well above the primary trend, near-record levels, positive RSI momentum — is the definitional bull market posture. Every scary headline hitting the tape this week should be evaluated against that baseline. The Iran peace deal signing today removes a genuine macro overhang that had weighed on energy costs, consumer sentiment, and Fed flexibility for over three months. Easing energy prices are disinflationary, which is precisely what the Fed needs to avoid the rate hike that half its committee is now penciling in. The market's 11-week winning streak already began pricing this resolution in; today's formal signing is confirmation, not news.

The Fed's hawkish dot plot flip deserves careful analysis rather than alarm. Yes, nine officials now see a rate hike before year-end — a meaningful shift from March's median projecting a cut. But what the market is actually doing tells you far more than what Fed officials forecast they might do. The S&P 500 absorbed Wednesday's hawkish press conference, gapped lower Thursday on the initial shock, then recovered sharply to close the week up 0.9%. That is the market rendering its verdict: monetary policy signals have shifted but not to a level that threatens the primary uptrend. The interest rate environment, while no longer accommodative, shows a 10-year/3-month spread still positive — the inversion that historically precedes recessions has not occurred, and both real-time GDP trackers are running solidly above 2.5%. The two-signal convergence that defines a recessionary bear — a grinding market decline plus deteriorating economic leading indicators — simply is not present. One leg of a potential warning is twitching; neither is flashing.

Accenture's historic single-session collapse and the Apple-Intel chip partnership together tell a coherent story about where capital is flowing within the technology complex. The IT consulting model built on billable human hours is facing a structural repricing as agentic AI tools automate work that previously required large teams — that is a genuine sector-level shift and the Accenture selloff is a legitimate single-stock signal for the traditional services space. But notice what happened simultaneously: the Philadelphia Semiconductor Index hit a record high. Capital is not fleeing technology; it is rotating within it — from labor-intensive services toward hardware infrastructure, domestic manufacturing, and the companies building the compute layer that makes AI possible. That is not a bear market signal. That is a healthy, functioning equity market repricing relative winners and losers within a still-expanding AI capital cycle. Employment conditions remain firm, consumer spending data has been upbeat, and the broader labor market signals show no meaningful deterioration — the employment backdrop that historically accompanies recessionary declines is absent.

The aggregate picture maps cleanly to the most favorable cell of the analytical framework: market above its primary trend, no recession confirmation, positive monetary policy spread, solid growth nowcasts, and easing geopolitical risk. The correct posture is fully invested. The pullback from the June 2 all-time high is just over 1% — not a correction, barely a ripple. Historically, all-time highs are associated with above-average forward returns, and there is no basis in the current data to treat this week's Fed hawkishness, Accenture's collapse, or even the Iran deal's implementation risks as reasons to reduce equity exposure. The one thing worth monitoring: if the inflation the Fed is flagging proves sticky enough to push rate hike expectations beyond one 25-basis-point move this year, and if growth trackers simultaneously begin to soften, that convergence would deserve attention. Right now, neither condition is met. Stay the course. MoreLess