The Ticker

Bull Market

The bull is still stomping around the pasture like he owns the place — a little spooked by the new sheriff in town, but with green grass underfoot, oil prices rolling back downhill, and chip factories lighting up coast to coast, this market's got more trot left in it than the bears want to admit.

Top Story

Warsh's Hawkish Fed Debut Rattles Wall Street & Signals Possible Hike

Wall Street woke up Thursday still digesting the most consequential Federal Reserve meeting in years — one that sent stocks tumbling and signaled that the era of easy money may be firmly behind us. New Fed Chair Kevin Warsh held rates steady at his inaugural FOMC meeting Wednesday but delivered a pointed inflation warning and stood back while half his committee penciled in a rate hike before year-end.

The broader earnings picture heading into this Fed regime shift remains constructive. Tech and semiconductor names are powering ahead — Intel has surged more than 200% this year, and the newly announced Apple partnership adds a landmark foundry win that validates its manufacturing renaissance. Strong retail sales data and a still-solid labor market suggest corporate top lines have held up reasonably well, even as margin pressures from persistent import inflation gnaw at the edges.

Warsh's press conference offered a sharp departure from the measured, forward-guidance-heavy style of his predecessor. He stripped the policy statement of its guidance language, declined to submit his own dot-plot forecast, and announced task forces to overhaul the Fed's communications, balance sheet, and inflation framework. Markets got fewer answers than they wanted, but the message on price stability was unmistakable: the new chairman views the Fed's five-year inflation miss as a credibility failure demanding correction, and he is prepared to hike if the data demands it.

The key macro wildcard now sits in the Middle East. The U.S.-Iran memorandum of understanding signed at Versailles on Wednesday opens a 60-day negotiating window, with the Strait of Hormuz set to reopen to free passage. If energy prices continue to fall, the inflationary pressure that is pushing Warsh toward tightening could ease meaningfully — potentially giving the Fed cover to hold rather than hike. That dynamic, more than any single data release, will define the monetary policy trajectory for the rest of 2026. MoreLess

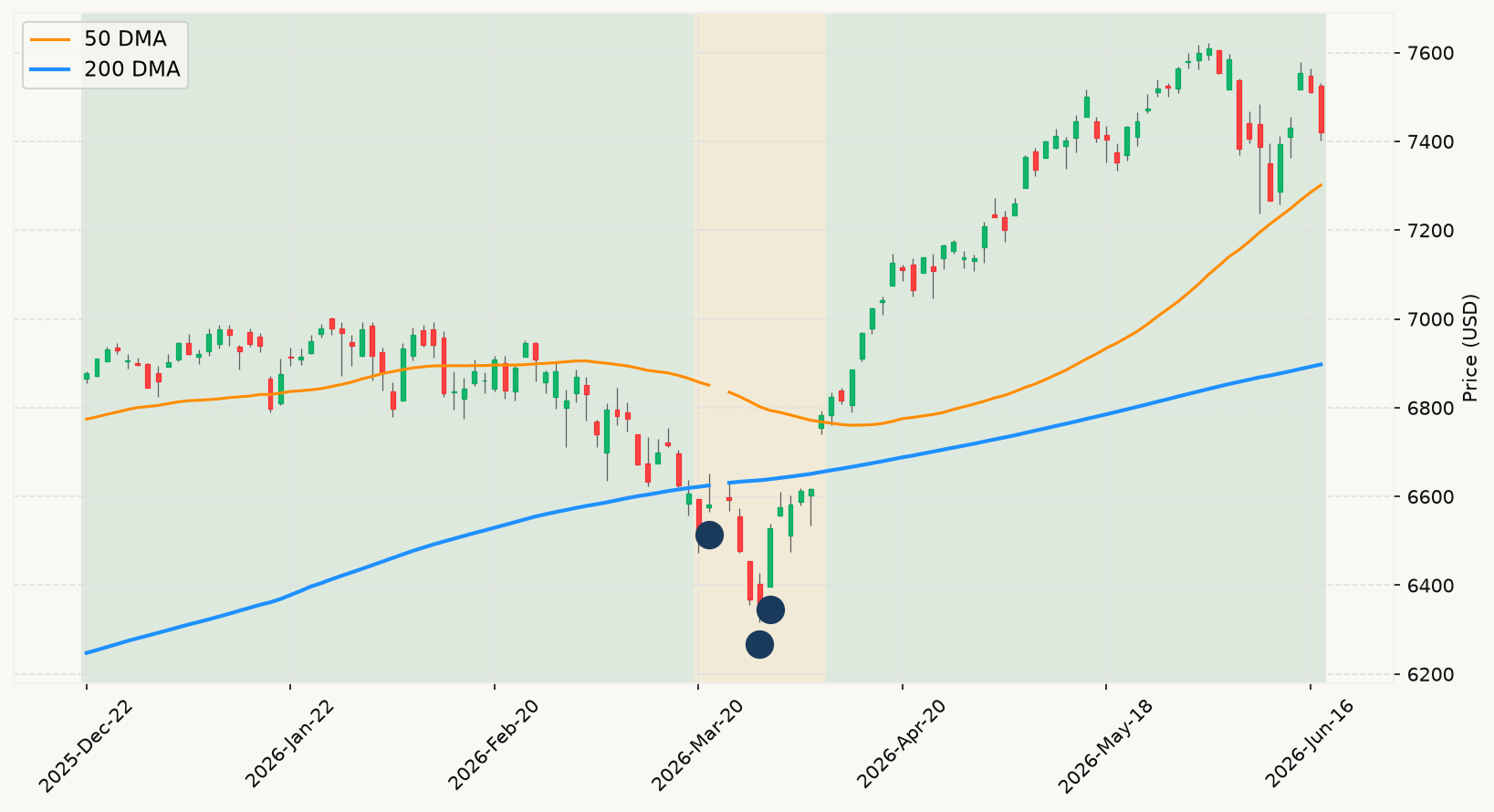

Six Month Chart (SPX)

⊞ Expand

The Ticker Analysis

Bull Market Intact — Warsh Noise, Not a Signal

The market's primary trend is firmly bullish — the S&P 500 sits well above its long-term stock market trend, the all-time high is a mere 16 days in the rearview mirror, and the drawdown from that peak is a slim 2.5%. That's not a warning signal; it's a routine consolidation within a functioning bull market. The Warsh Fed shock that hammered stocks on Wednesday afternoon is exactly the kind of headline-driven volatility the historical data consistently classifies as noise. A single bad FOMC day, however jarring, has zero predictive value for where the market sits six months from now. The price action this morning — futures rebounding, chip stocks surging — is precisely what you'd expect when a sentiment-driven air pocket meets an otherwise intact underlying trend.

The recession checklist deserves an honest read given the hawkish pivot now embedded in market pricing. On the interest rate environment: the yield spread between the 10-year and 3-month Treasury remains positive, which means the monetary policy signals are not yet flashing the inversion warning that has preceded every modern U.S. recession. Employment conditions are equally benign — weekly claims near 226,000 are historically low, the Philly Fed employment gauge just jumped back into expansion territory, and labor market signals show no sign of the deterioration that would constitute the second leg of a recession confirmation. The nowcasts confirm it: both growth trackers are running solidly positive for Q2. You would need to see a meaningful deterioration across multiple leading indicators simultaneously before the analytical picture changes. Right now, that convergence simply isn't there.

The Iran peace deal is the most consequential macro development beyond the Fed. If the Strait of Hormuz reopens and energy prices continue their descent — WTI is already back near $75 — headline inflation could cool meaningfully over the next two to three months. That matters enormously for the Fed's calculus. Warsh's hawkish dot plot was built on an inflation backdrop partially fueled by the Middle East conflict. A durable energy price decline could render the rate-hike scenario less probable than the market is currently pricing, which would shift the interest rate environment back in equities' favor. This is exactly the scenario where the market's own price action — not the news — will tell you which way the evidence is breaking. Watch the trend, not the narrative.

The Apple-Intel chip announcement adds a layer of structural bullishness to the secular technology story. The broadening of domestic semiconductor manufacturing capacity, backed by federal equity stakes and a reshoring industrial policy, represents a durable earnings tailwind for the sector that cuts across geopolitical risk. For investors positioned in diversified equity index funds — the only sensible vehicle given the historical evidence that 59% of individual stocks underperform Treasury bills over their lifetimes — this is the kind of systemic, macro-level shift that gets fully captured without any need to pick winners within the space. The current positioning prescription is unchanged and unambiguous: stay fully invested, monitor the primary market trend and leading economic indicators for any sign of convergence toward recession confirmation, and treat Wednesday's FOMC-driven selloff for what it is — a bump on a road that is still pointing up. MoreLess