The Ticker Analysis

Bulls Rule — Stay Invested, Ignore the Fed Theater

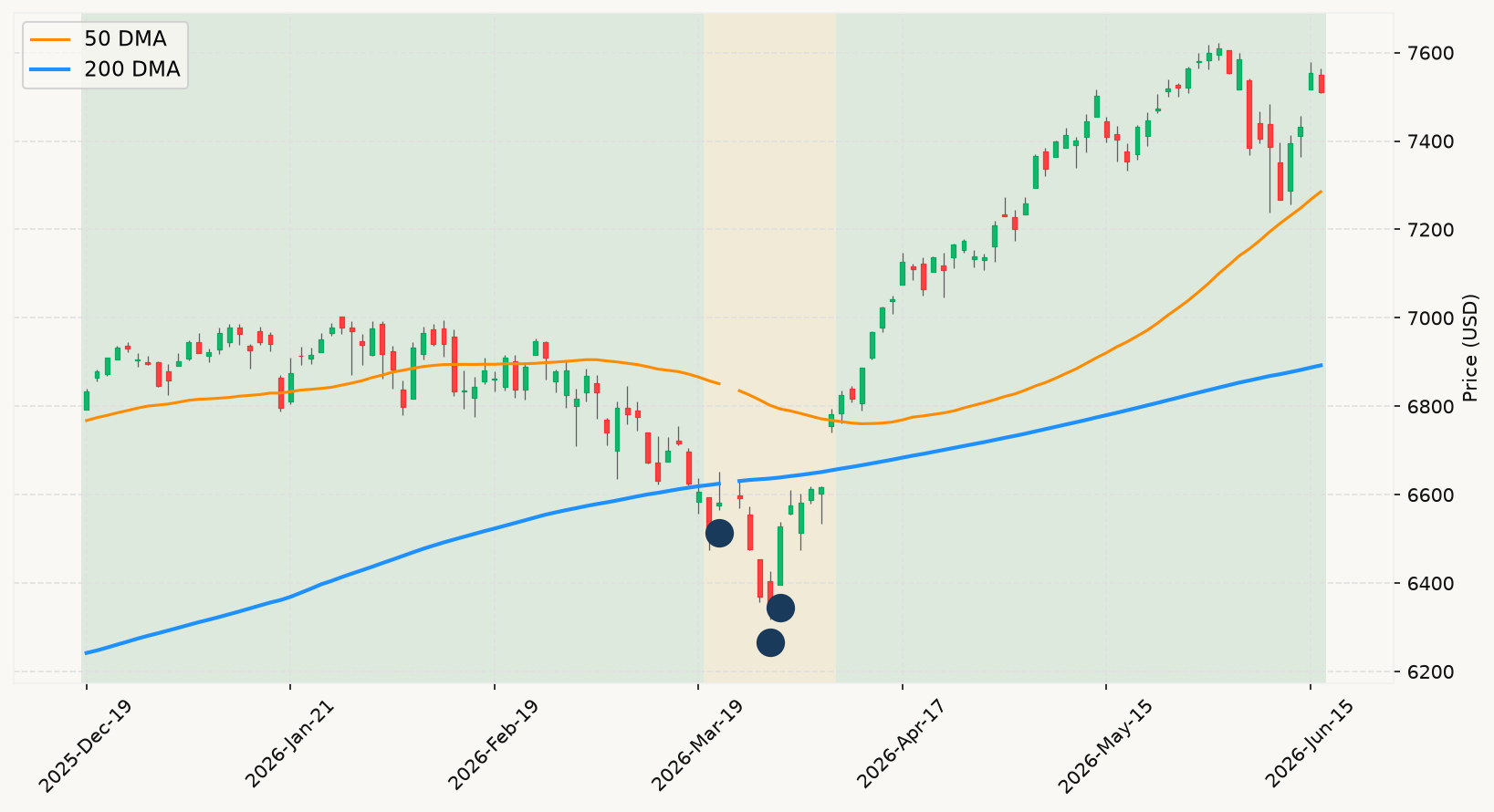

The top story today — Warsh's Fed debut and the dot-plot reckoning — is market noise dressed up as a signal, and the distinction matters enormously. The rate decision itself is fully priced; a hold changes nothing about the primary market trend, which remains unambiguously above its long-run trend line. What the market is actually doing — sitting just 1.3% below an all-time high set 15 days ago, with futures pointing up this morning — is the most important piece of information available. The hand-wringing over whether the June dot plot erases the last projected cut is exactly the kind of narrative churn the analytical approach here treats with deep skepticism. Policymakers removing a phantom cut from their projections is not the same thing as tightening policy. The interest rate environment, while restrictive, has been stable across four consecutive holds — and a stable environment is not a deteriorating one. There is no convergence of signals here pointing toward economic contraction.

The semiconductor selloff is a more interesting case, and the framework resolves it cleanly. Yes, Nvidia, AMD, Intel, and Broadcom got hit hard on Tuesday. But look at the cause: profit-taking after a monster run, amplified by a modestly hot CPI print and a Broadcom guidance figure that came in below the stratospheric bar analysts had set. This is textbook fast-money rotation, not a structural repricing of the AI thesis. Hyperscalers have committed $750 billion in capital expenditures for the year — that demand floor hasn't moved. The sector is bouncing in pre-market trade right now. Fast, sharp sector declines that reverse within days are the market clearing froth, not sounding an alarm. The stock market trend is bullish. One rough Tuesday in semis doesn't change that verdict.

The BMW profit warning deserves a closer look because it touches real macro variables — China demand destruction and Middle East conflict spillovers — that could, in theory, feed into broader economic deterioration. The key question is whether this is idiosyncratic European auto-sector stress or a leading indicator of something wider. The data points against the latter interpretation. U.S. labor market signals remain healthy, both GDP tracking models are running well above stall speed, and the monetary policy environment — while not accommodative — is not actively tightening. BMW's pain is real, but it is concentrated in combustion-engine vehicle demand in China and energy-cost sensitivity in Europe — not the U.S. consumer, not U.S. corporate earnings broadly, and not U.S. credit conditions. The framework watches for convergence across multiple leading indicators simultaneously. One European automaker's guidance cut does not move that needle.

The SpaceX-Cursor deal is pure noise from an analytical standpoint, but it does illuminate something useful about the current market regime. The fact that a company can go public at a $1.77 trillion valuation, watch its stock surge roughly 50% in four trading days, and then immediately deploy that currency in a $60 billion all-stock acquisition tells you the risk appetite in this market is running very hot. That is not a warning — the data shows all-time highs are historically associated with above-average forward returns, not exhaustion. But it is context. The market is fully invested in the upside narrative right now, which means the margin for disappointment from today's Warsh press conference is higher than usual. A hawkish tone that surprises to the upside could generate intraday volatility. The posture remains fully invested. Volatility around a Fed press conference is not a reason to move to the sidelines — it is, at most, a reason to not check your portfolio at 2:31 PM. MoreLess