The Ticker Analysis

Bull Trend Intact — Stay Invested, Ignore the Noise

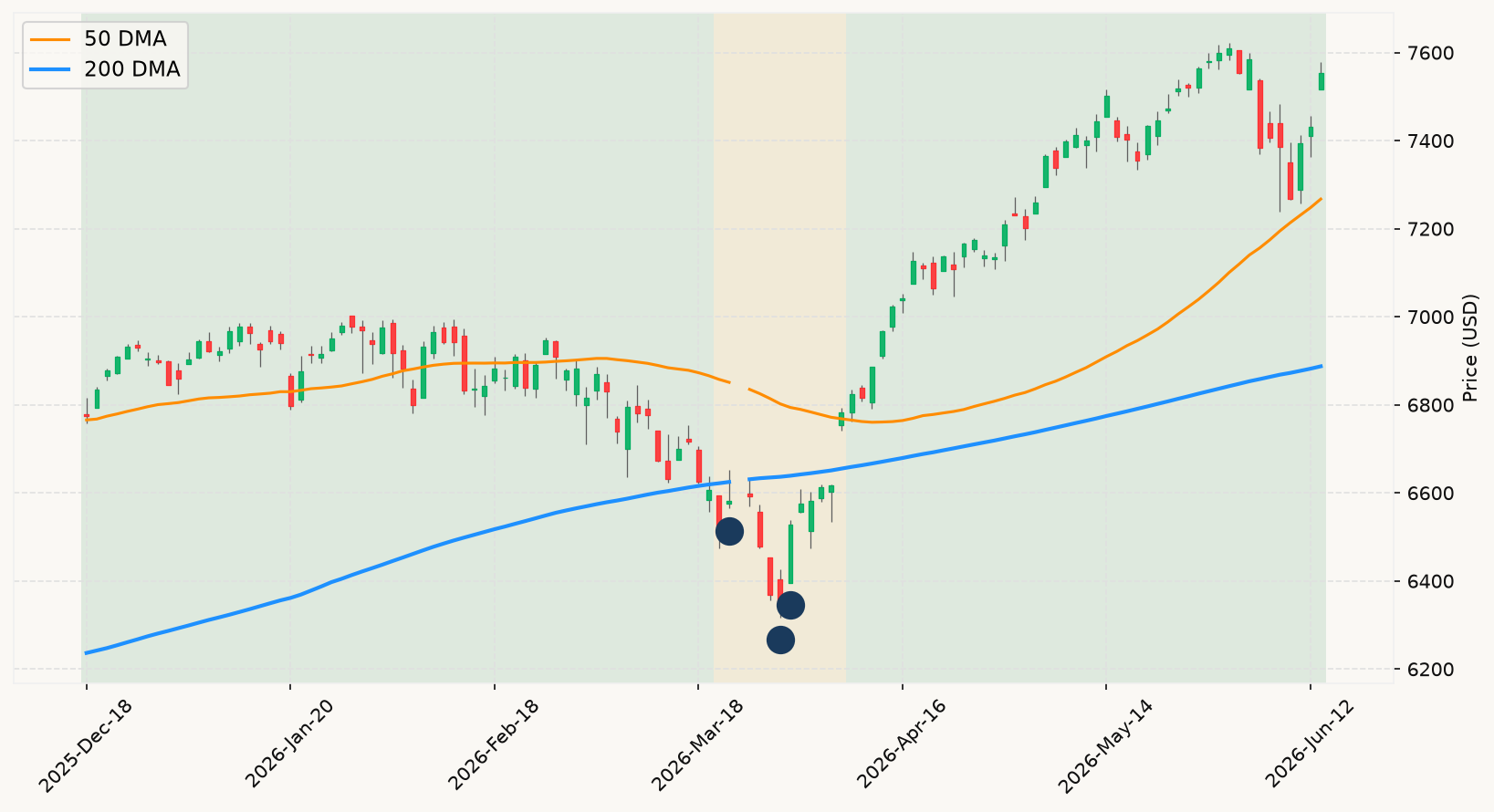

The US-Iran deal and the reopening of the Strait of Hormuz is exactly the kind of headline that generates enormous emotional weight — but within a disciplined analytical lens, it is noise dressed up as signal. The market was already comfortably above its primary trend line before the deal, meaning the bull trend was intact regardless. Geopolitical resolutions are not structural inflection points for equity markets unless they were themselves the cause of a sustained break below trend — and the Strait closure, while disruptive, never produced that. The deal accelerates the unwind of an energy-price headwind, but that doesn't change the market regime: you were fully invested before this headline, and you stay fully invested after it. The relief rally is pleasant confirmation that the bullish trend is holding, not a new reason to participate.

The Kevin Warsh Fed meeting is generating enormous attention, and appropriately so — but not for the reasons most market commentary will emphasize. The rate decision itself is already priced in; a hold was essentially certain going into today. What matters for the analytical framework is what the updated dot plot and Warsh's inaugural press conference reveal about the trajectory of real rates and the Fed's inflation tolerance. If the committee signals a neutral-to-hawkish pivot and removes explicit easing language, that does not itself constitute a recession signal — employment conditions remain healthy and the interest rate environment, while firm, shows no inversion of the kind that has historically preceded contractions. Watch for whether monetary policy signals shift from "on hold" to "next move is a hike," which would be a development worth monitoring — but even then, a single hawkish pivot is not the convergence of multiple deteriorating indicators that defines a genuine recession warning.

The SpaceX IPO and the Wells Fargo target upgrade are both firmly in the noise category as market-timing inputs. A landmark IPO tells you about sentiment and risk appetite — both currently elevated — but it carries no predictive weight for the broader index direction. Analyst target upgrades are even further down the list of things worth tracking; they are systematic post-hoc confirmations of moves already made, not leading indicators. What they do confirm, collectively, is that the earnings backdrop remains solid. Wells Fargo's upward revision to S&P 500 EPS estimates is consistent with what the market itself has been pricing: profit growth is holding up, and the economic expansion that drives it shows no signs of rolling over based on the high-frequency data flowing into the growth nowcasts.

Pulling back to the full picture: the stock market is above its primary trend, the fast-crash panic signal is inactive, employment conditions are healthy, and the interest rate environment — while no longer accommodating — is not sending contraction signals. Every cell in the decision matrix points to the same posture: stay fully invested. The BOJ rate hike is worth monitoring for any global carry-trade unwind effects, and the Warsh press conference tomorrow deserves close attention for its dot-plot implications — but neither event changes the current regime. The base rate here is overwhelmingly favorable: corrections that occur with the market above its primary trend, in the absence of recession confirmation, have resolved to the upside in the historical record with remarkable consistency. Nothing in today's tape overrides that evidence. MoreLess